Software-as-a-Service arrangements

I read the paper published in connection with current research of the IASB on intangible assets concerning Software-as-a-Service arrangements. Here is my easy-to-understand summary.

“Your company has both accounting and tax depreciation, as stated in the past year's process notes. How very interesting! Can you tell me more about it?"

The chief accountant did not bat an eye.

"We do. Probably much like every company here on earth."

I went back to the windowless chamber reserved for our audit fieldwork, red-faced with embarrassment.

It was day 5 of my first real audit at a car manufacturer. And I did not even know the basics of tax and accounting depreciation.

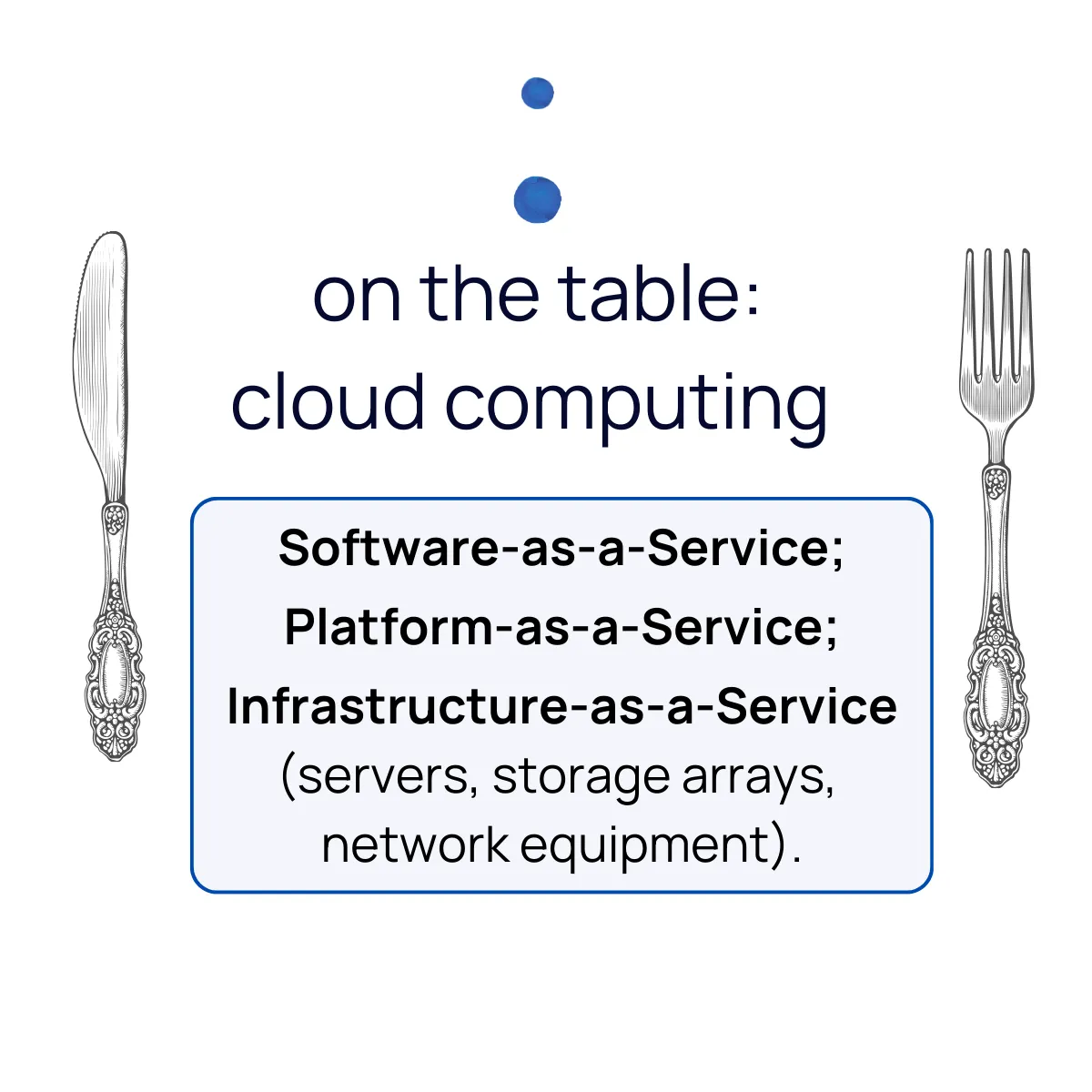

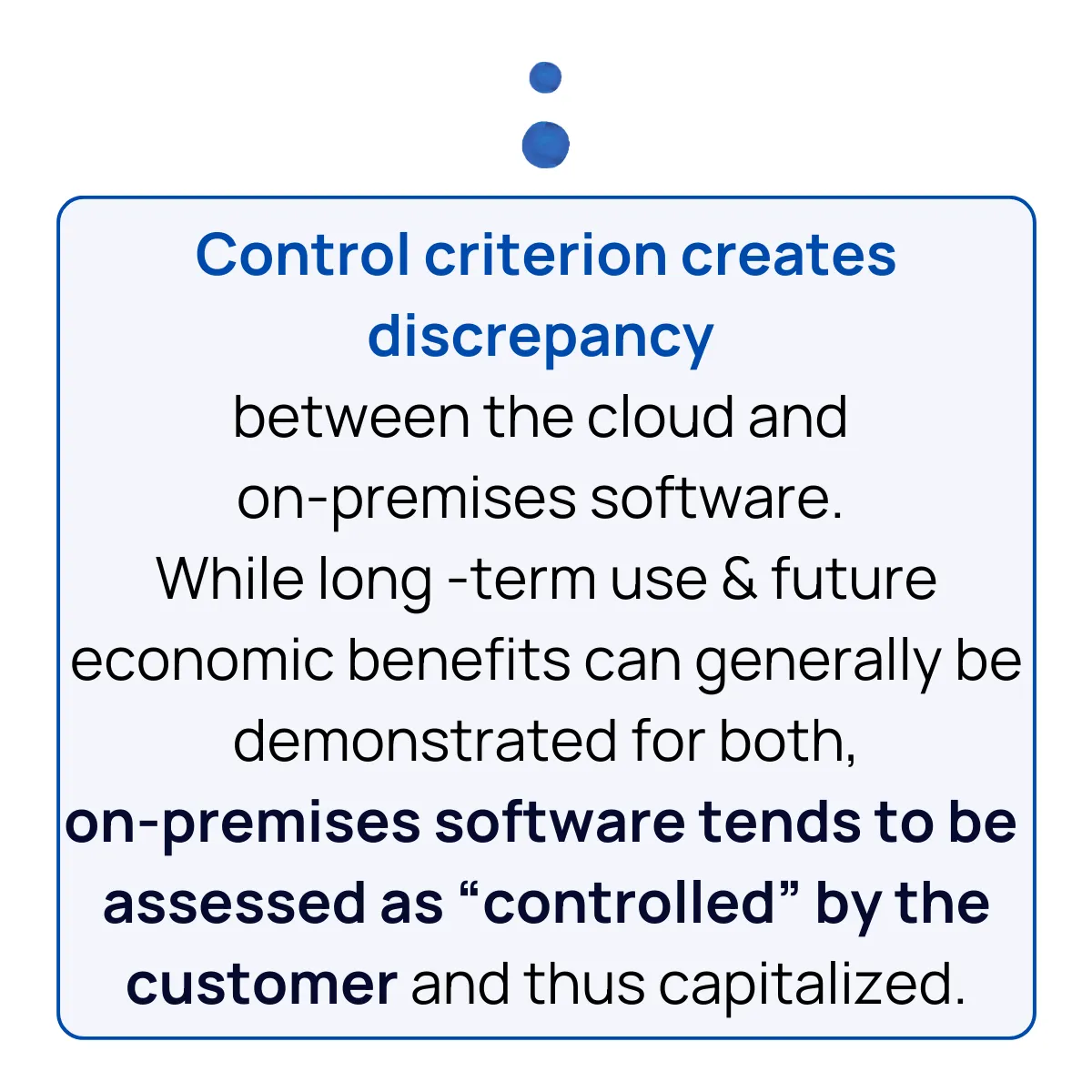

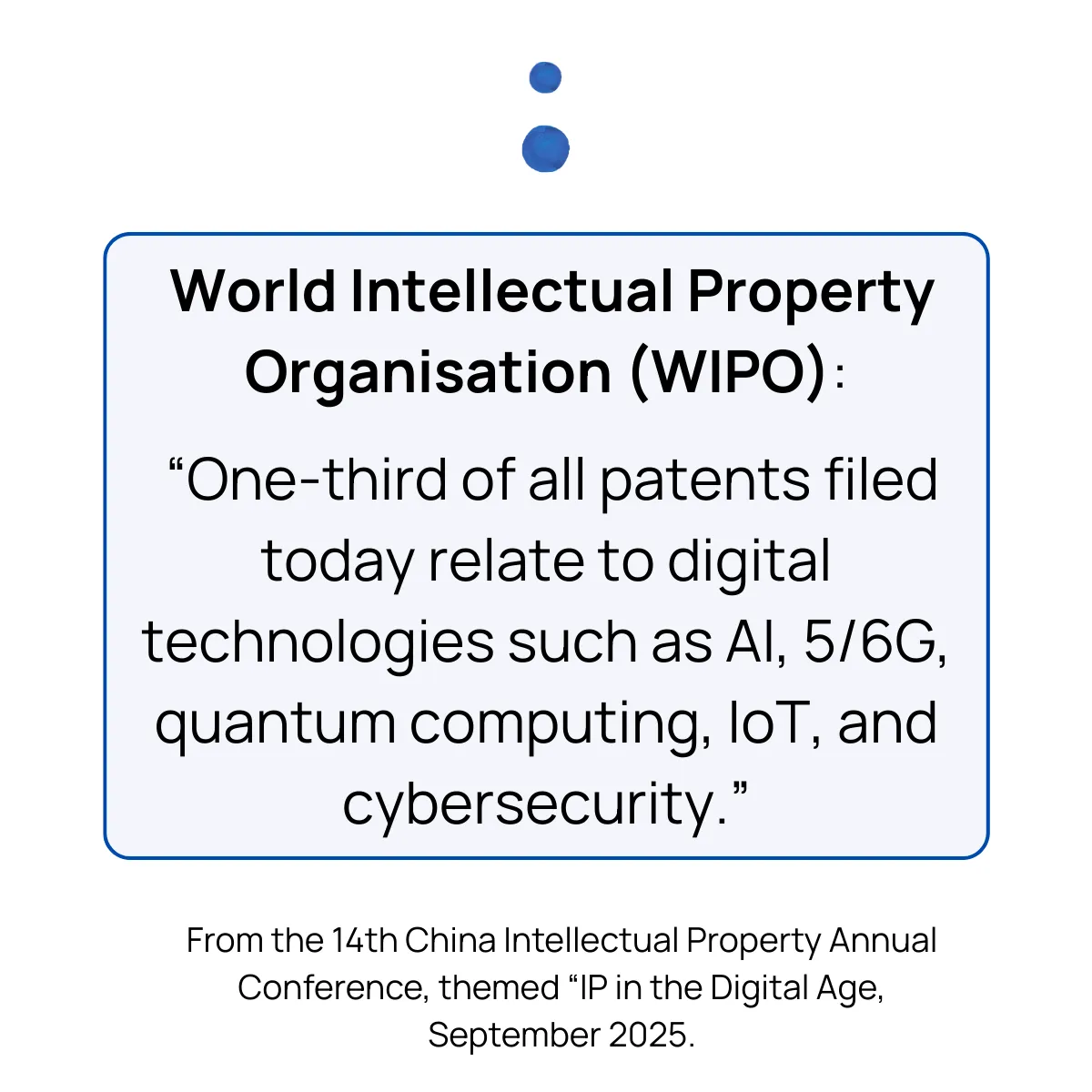

📍While difference between accounting and tax depreciation is obvious to any professional the difference between "on-premises" and "cloud" software arrangements might not be the case.

I read the paper published in connection with current research of the IASB on intangible assets concerning "Software-as-a-Service" arrangements.

⏩ Find my simple summary on the topic in the carousel.

Full paper is accessible here:

https://lnkd.in/eJrwetjs

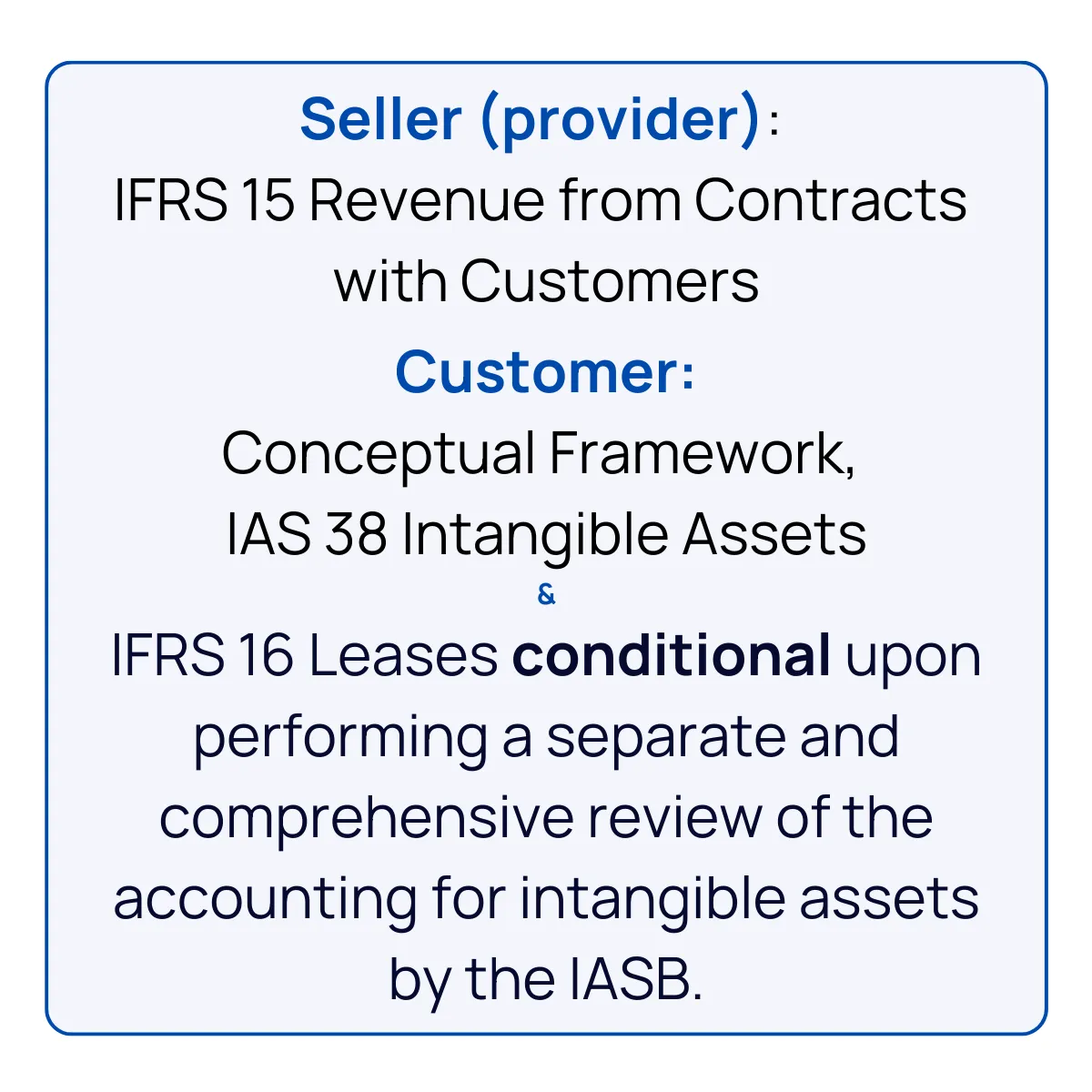

The research paper references two past IFRIC Agenda Decisions:

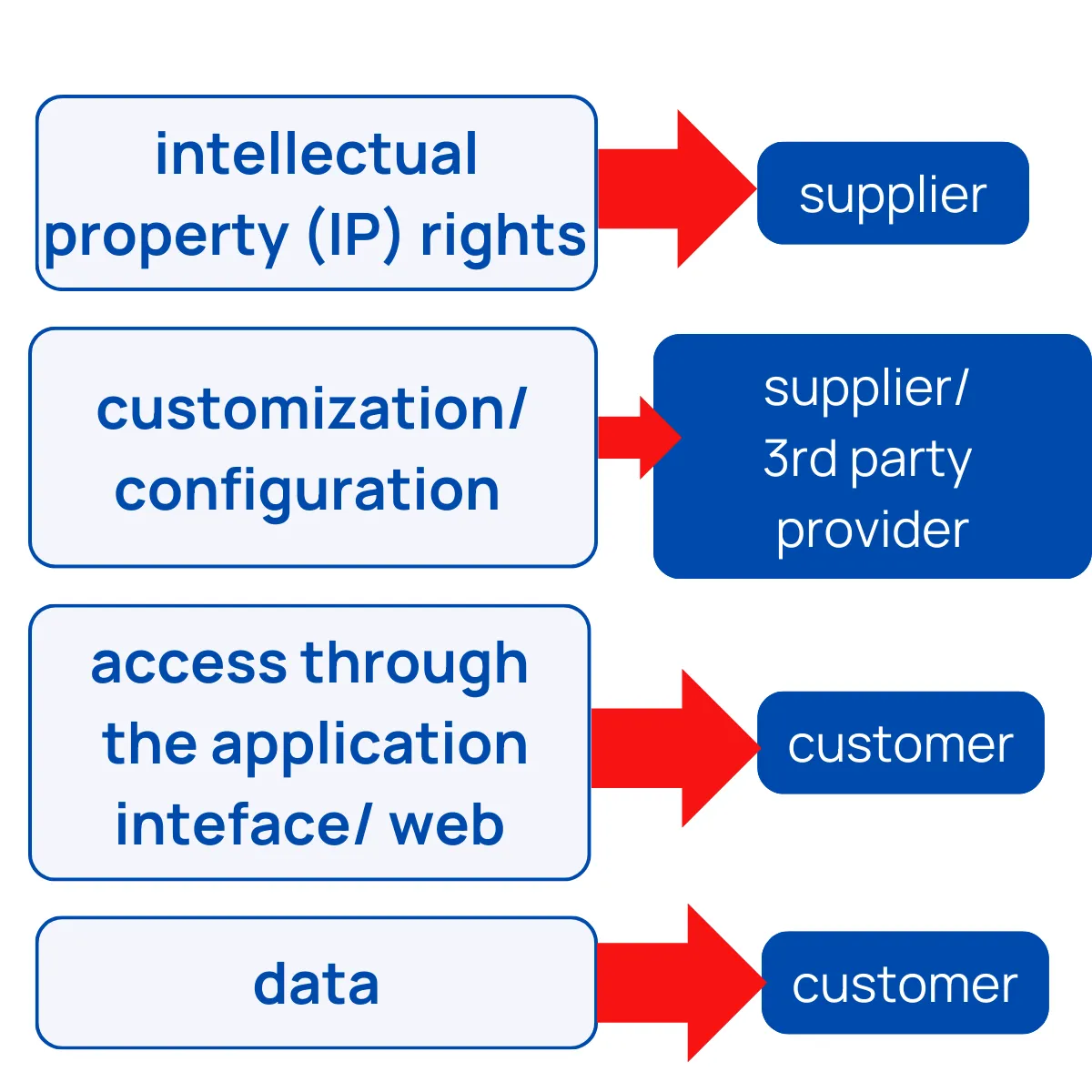

2019: Customer’s Right to Receive Access to the Supplier’s Software Hosted on the Cloud:

https://shorturl.at/p6h31

-> No intangible asset recognized. The customer receives an access to a service but lacks both the rights over the software (control element) and the future economic benefits.

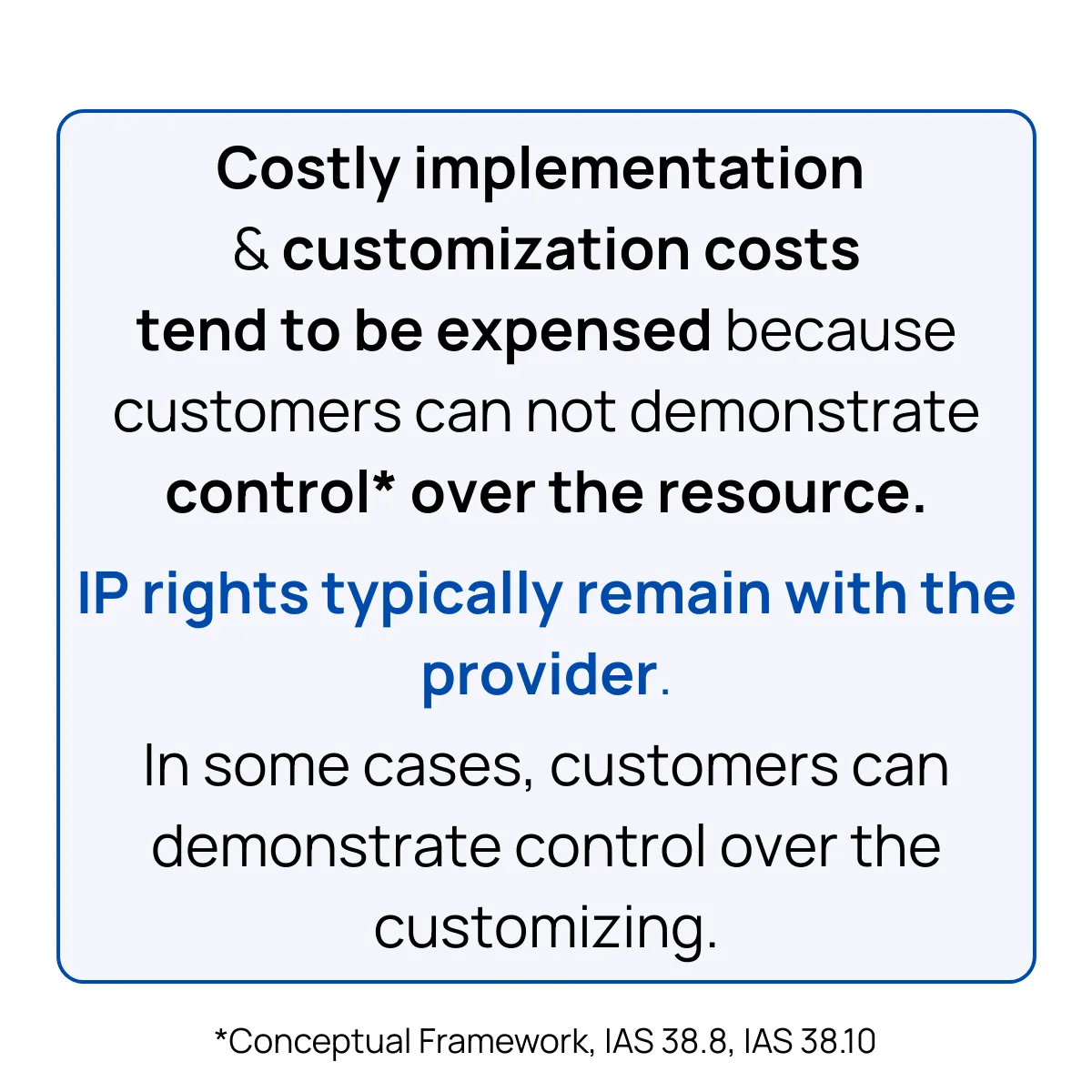

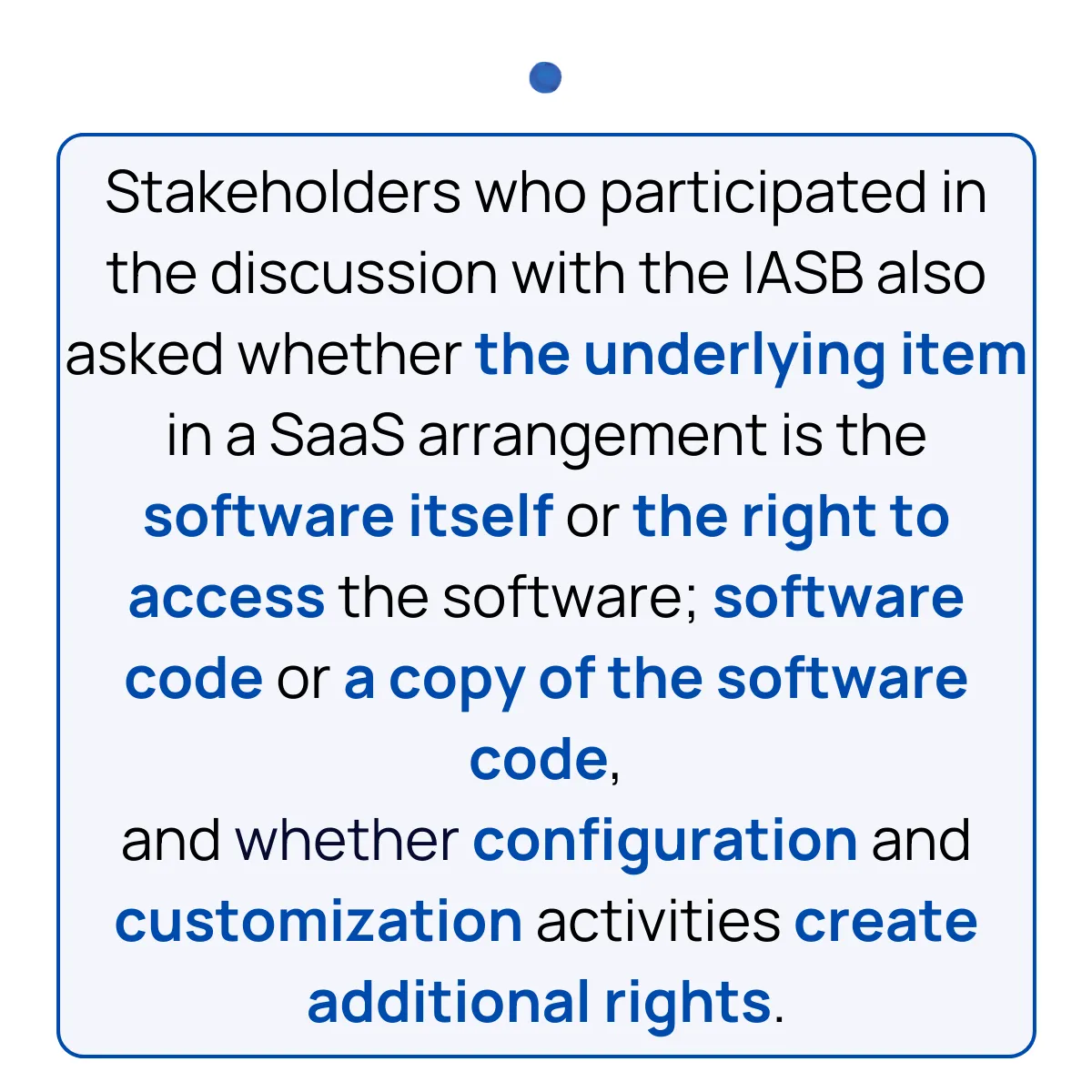

2021: Configuration or Customisation Costs in a Cloud Computing Arrangement:

https://shorturl.at/nq09y

No intangible asset recognized since the customer lacks control over the software, despite the fact the software had to be customized at the costs of customer.