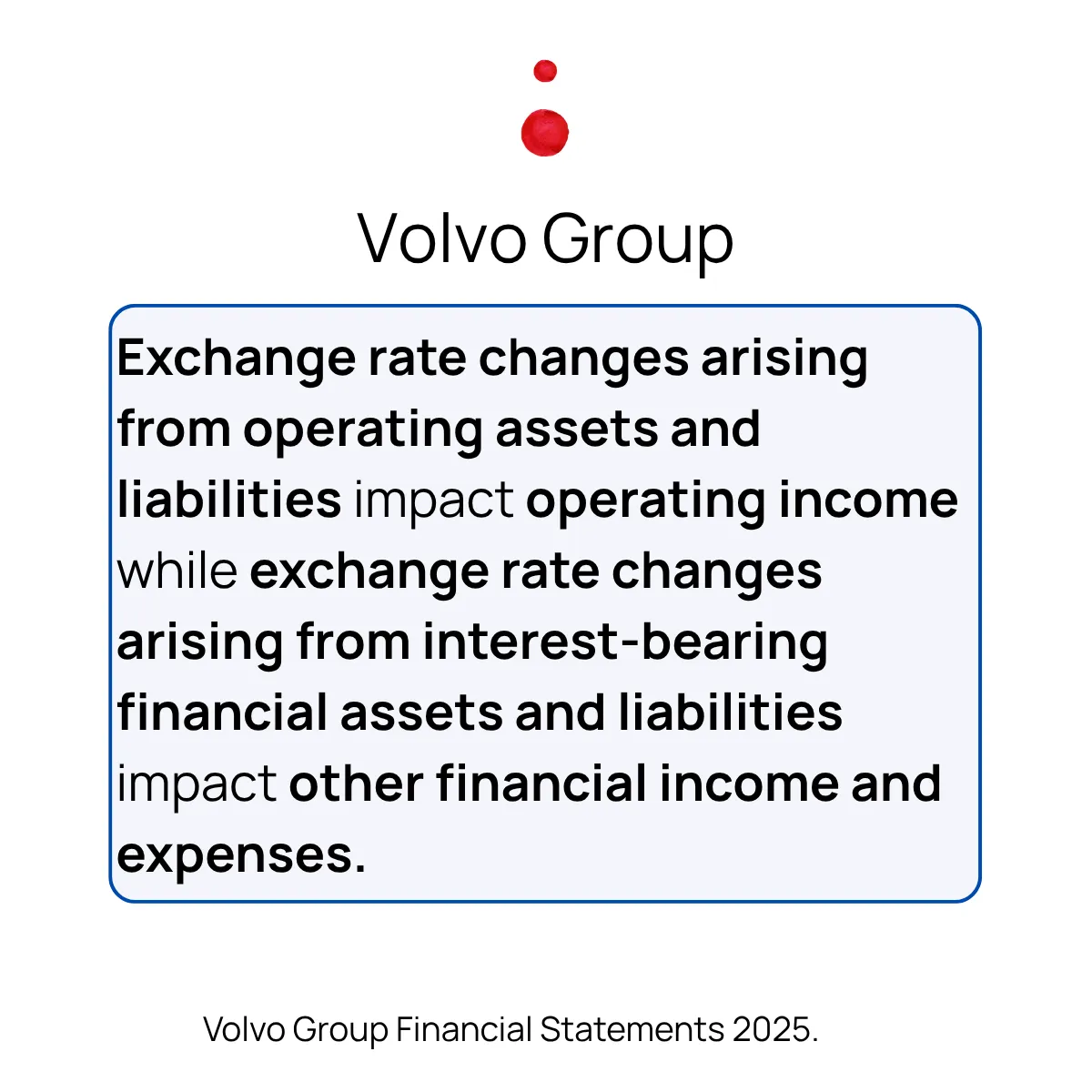

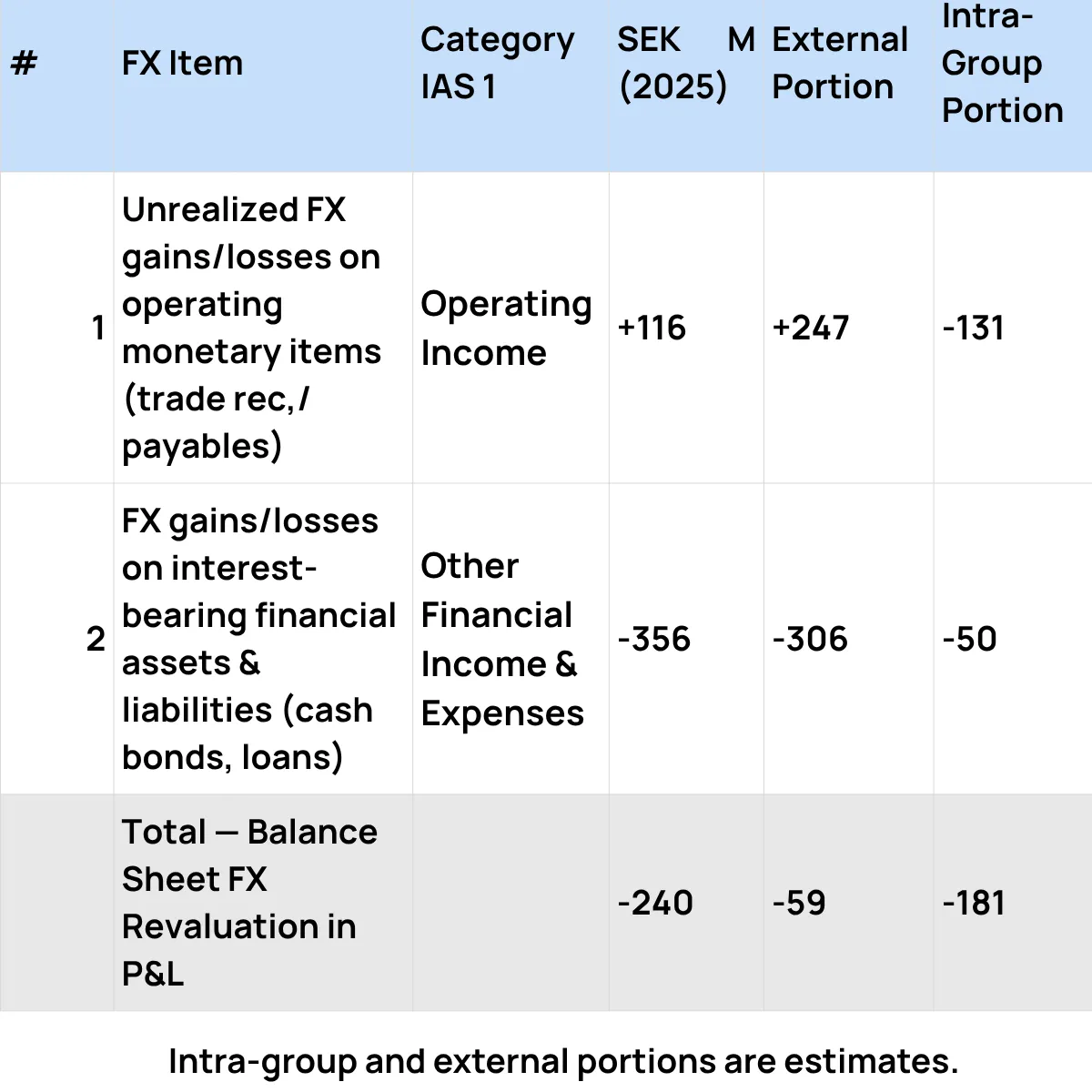

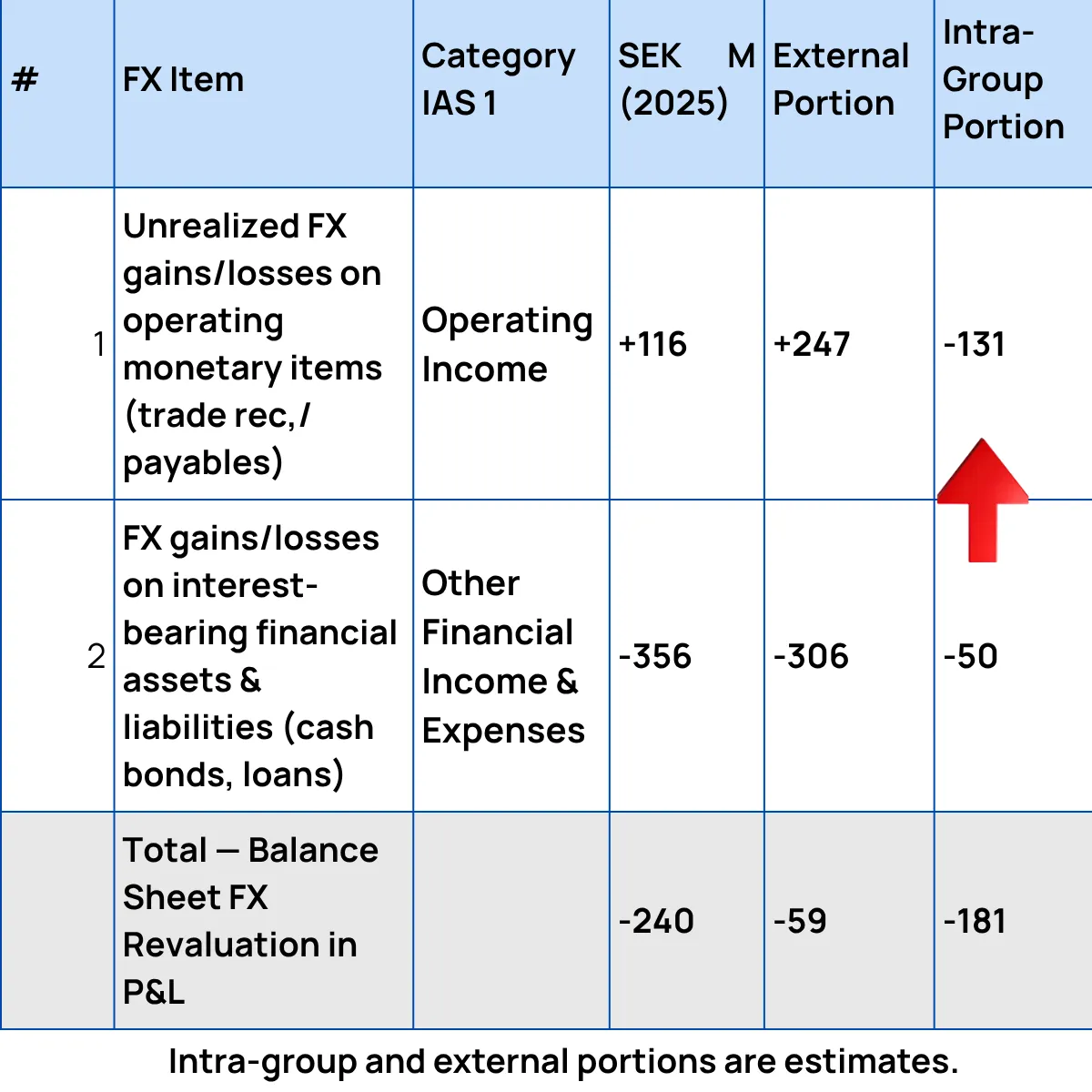

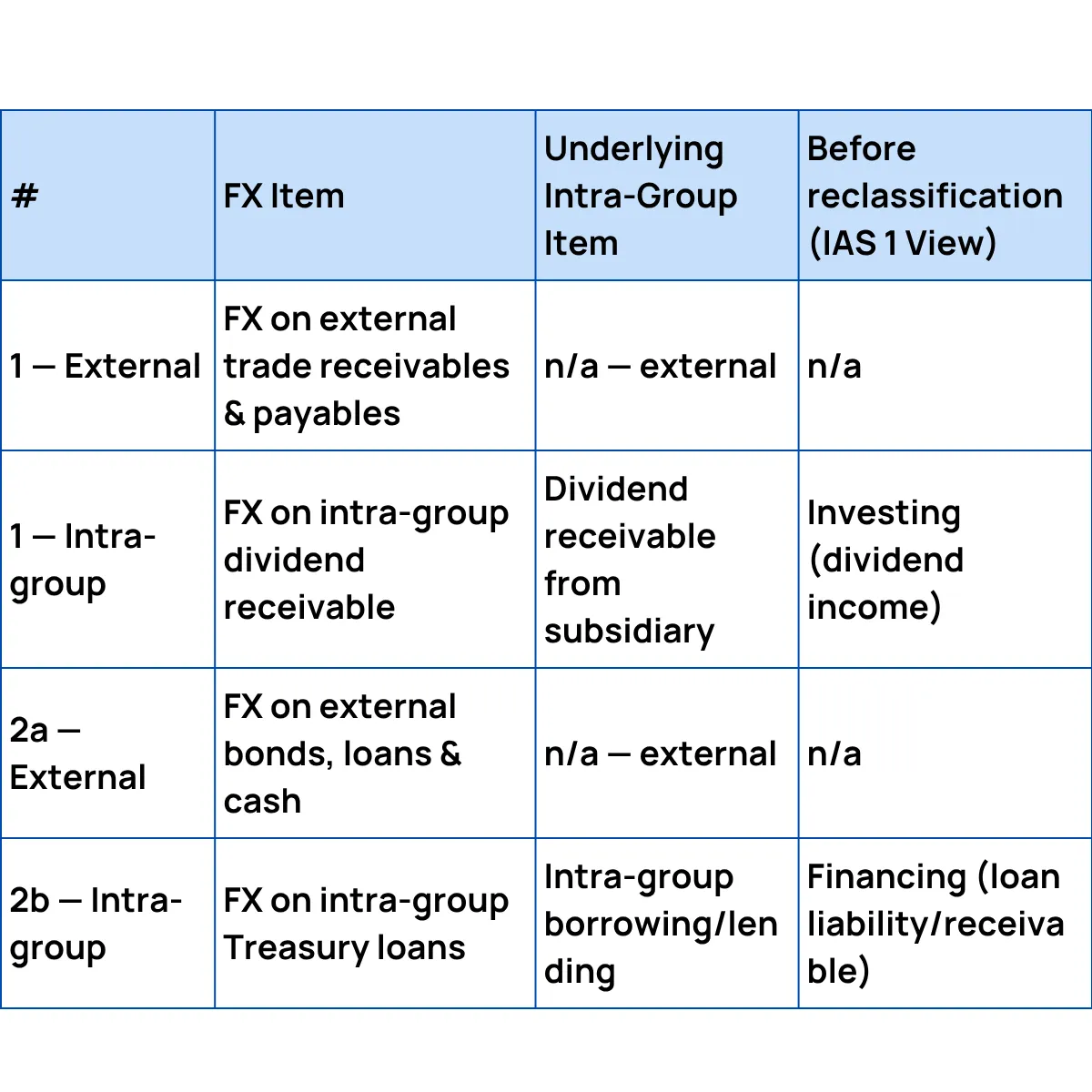

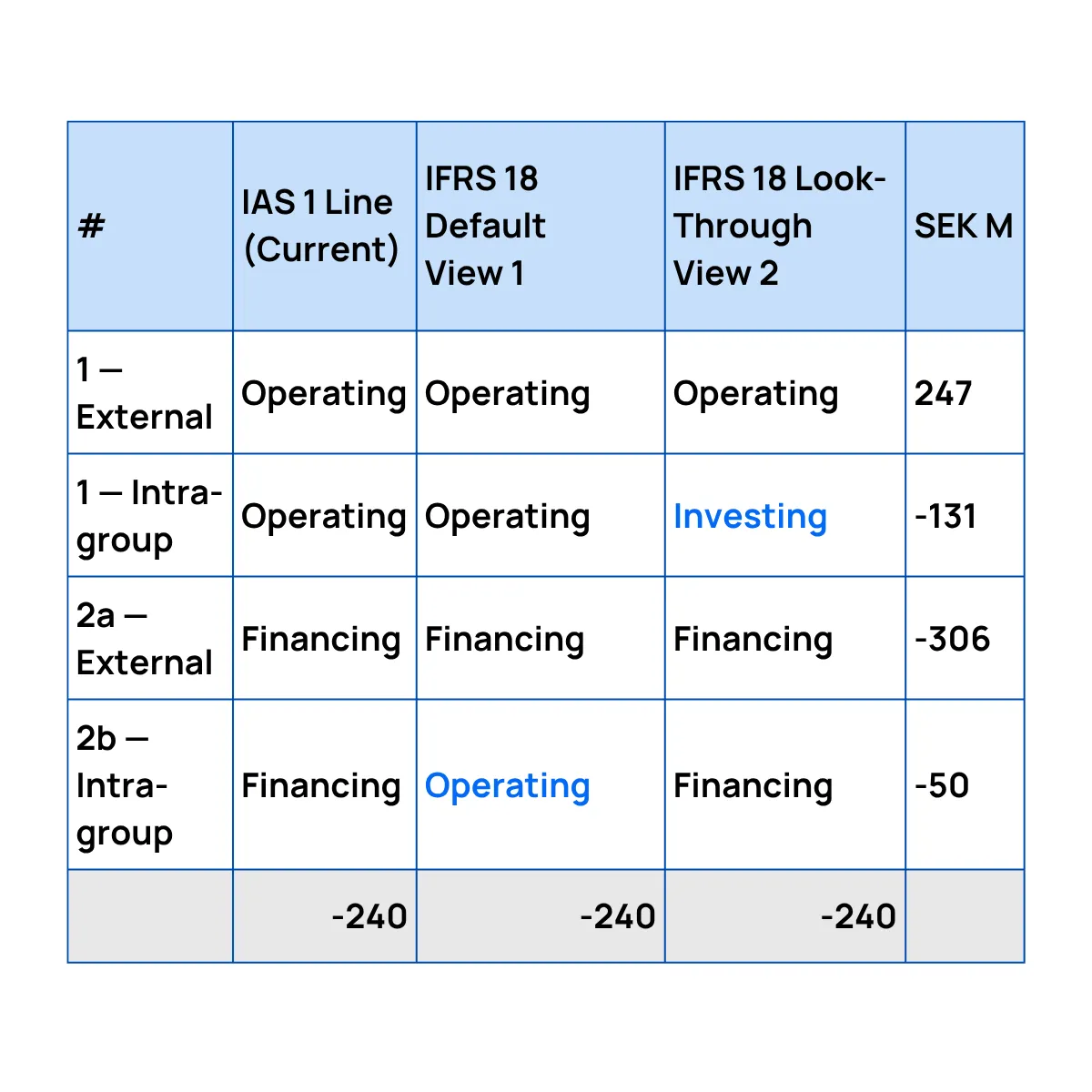

One-by-one or all? Foreign exchange differences on intragroup monetary items

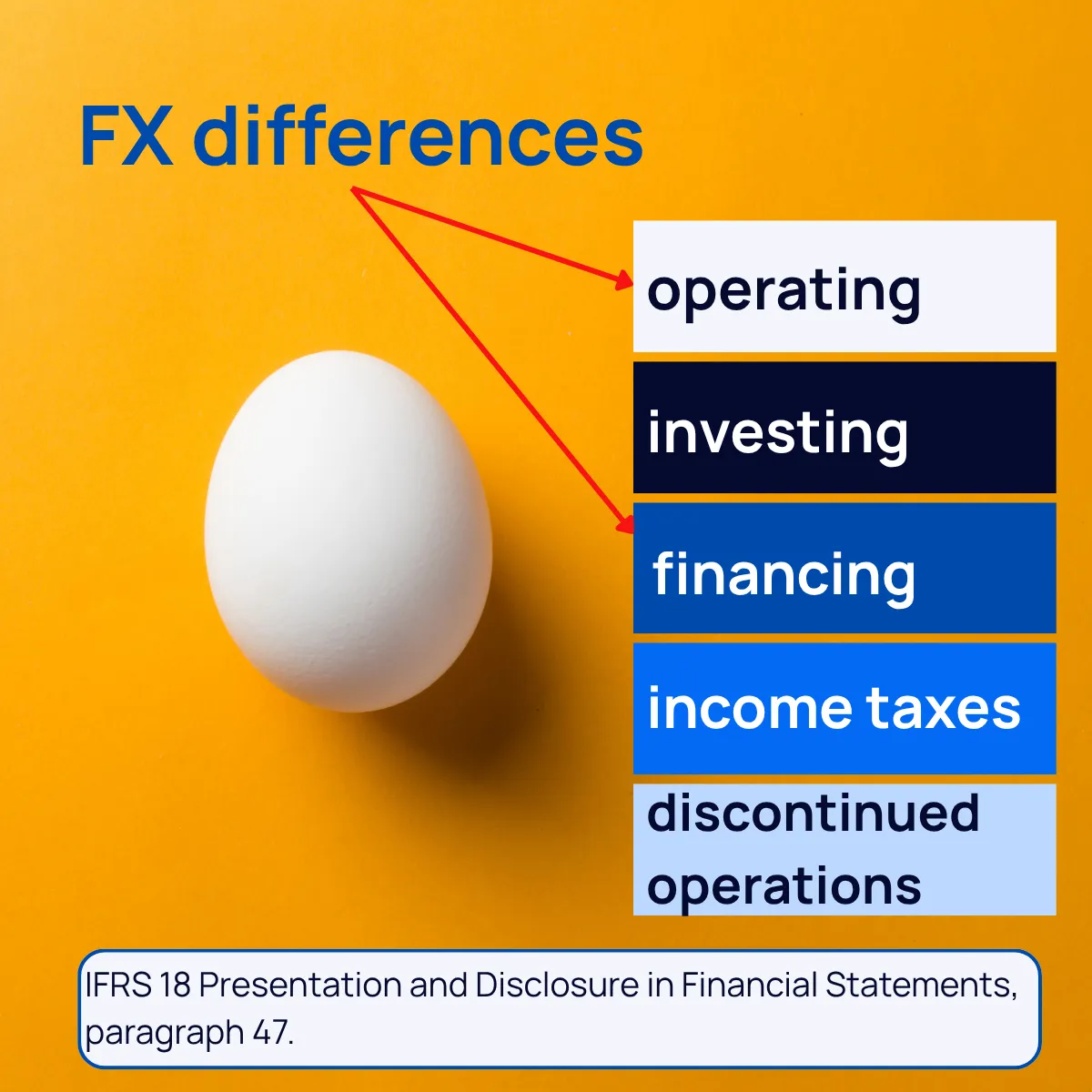

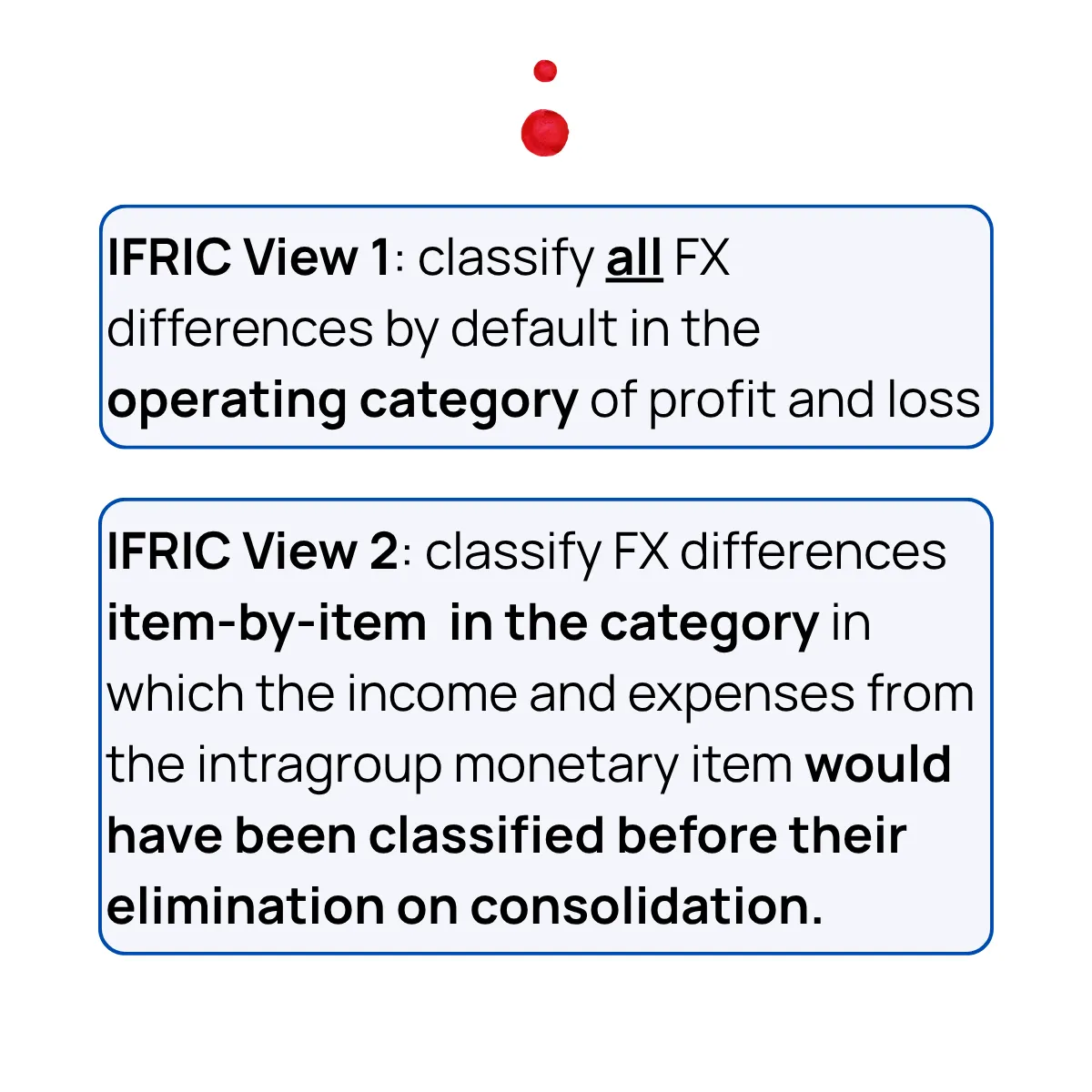

An entity might classify all FX differences in the operating category of profit or loss or opt for an item-by-item classification in the category in which the income and expenses on the intragroup monetary item would have been classified before their elimination on consolidation.

"All-in-one vs item-by-item." Have you thought about foreign exchange differences on intragroup monetary items (IFRS 18) in terms of “items count” or "volume"?

Only after I listened to this podcast summary from Brian O'Donovan from IFRIC it dawned on me: https://shorturl.at/9E5mV

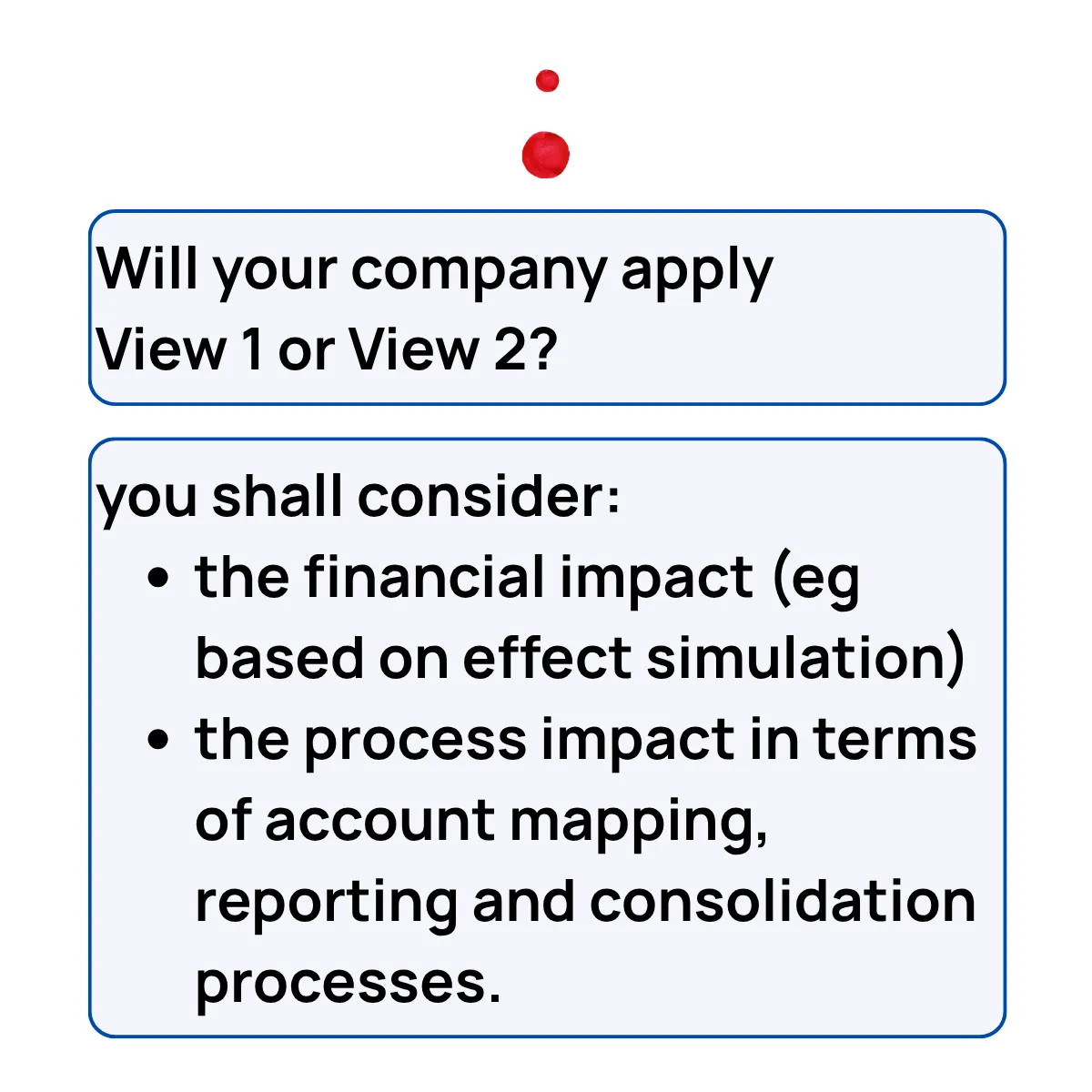

View 1 and View 2 shall also be considered by entities implementing IFRS 18 from the perspective of process complexity in terms of:

🔹 "one-by-one (decision making and classification)" vs. 🔹 "all-in-one (category)".

⏩ I hope today's carousel can illustrate the concept for you.

📍In addition, this is a perfect opportunity to „exercise“ an effect simulation with AI (I used Claude Sonnet 4.6).