IAS 28 Investments in Associates and Joint Ventures

IAS 28 prescribes the accounting for investments in associates and sets out the requirements for the application of the equity method when accounting for investments in associates and joint ventures.

"It is a scale of proportions that makes the bad difficult and the good easy."

My today's carousel is about IAS 28 Investments in Associates and Joint Ventures in just 15 seconds.

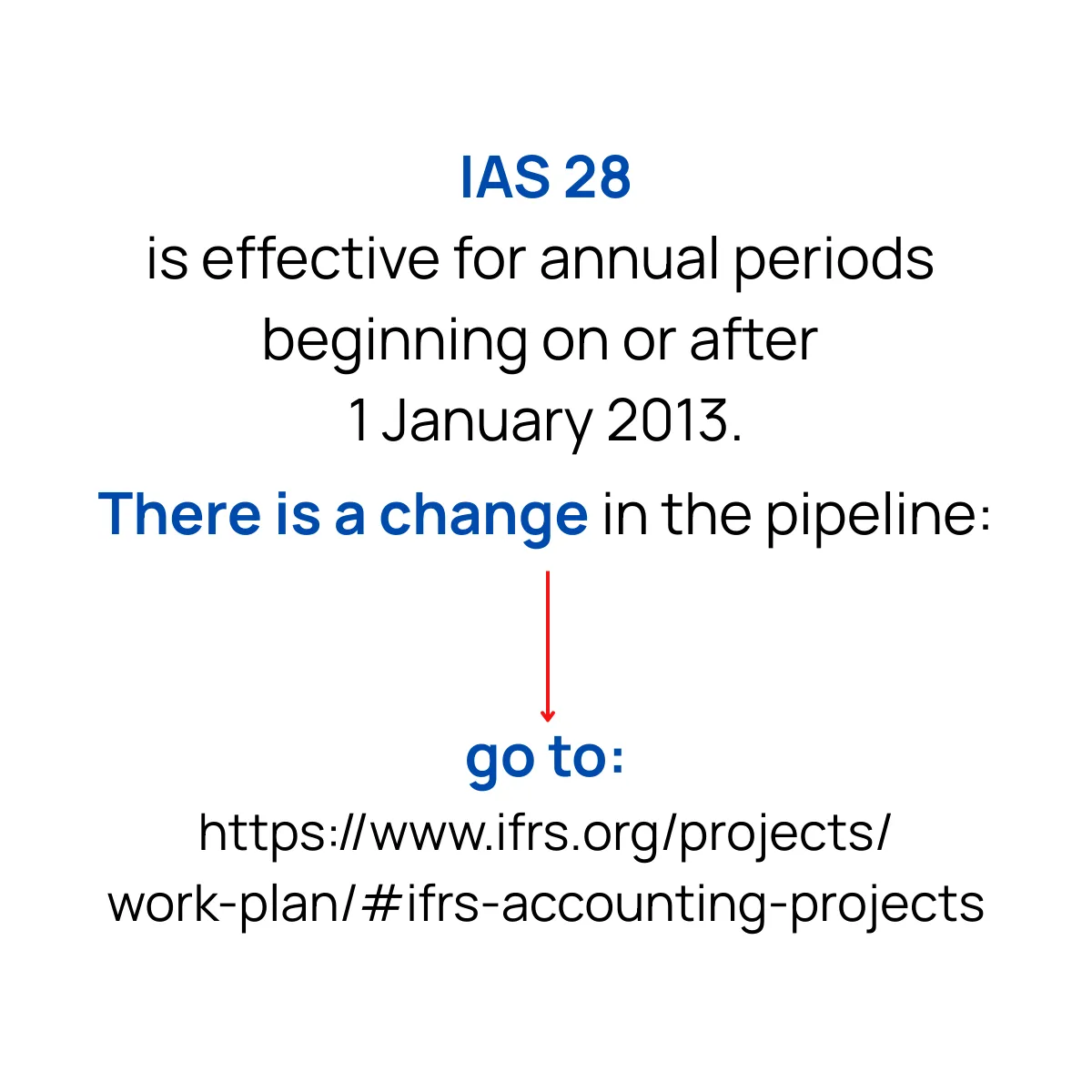

A project on IAS 28 is in the IASB project pipeline (project direction tbd in Q1 2026).

The primary objective is addressing various application questions & improving the understandability of IAS 28:

🔹How to measure the cost of an associate or a joint venture?

🔹When the investor obtains significant influence/ on which date an entity becomes an associate or a joint venture?

🔹Related to the determination of the date - when a change in ownership becomes effective?

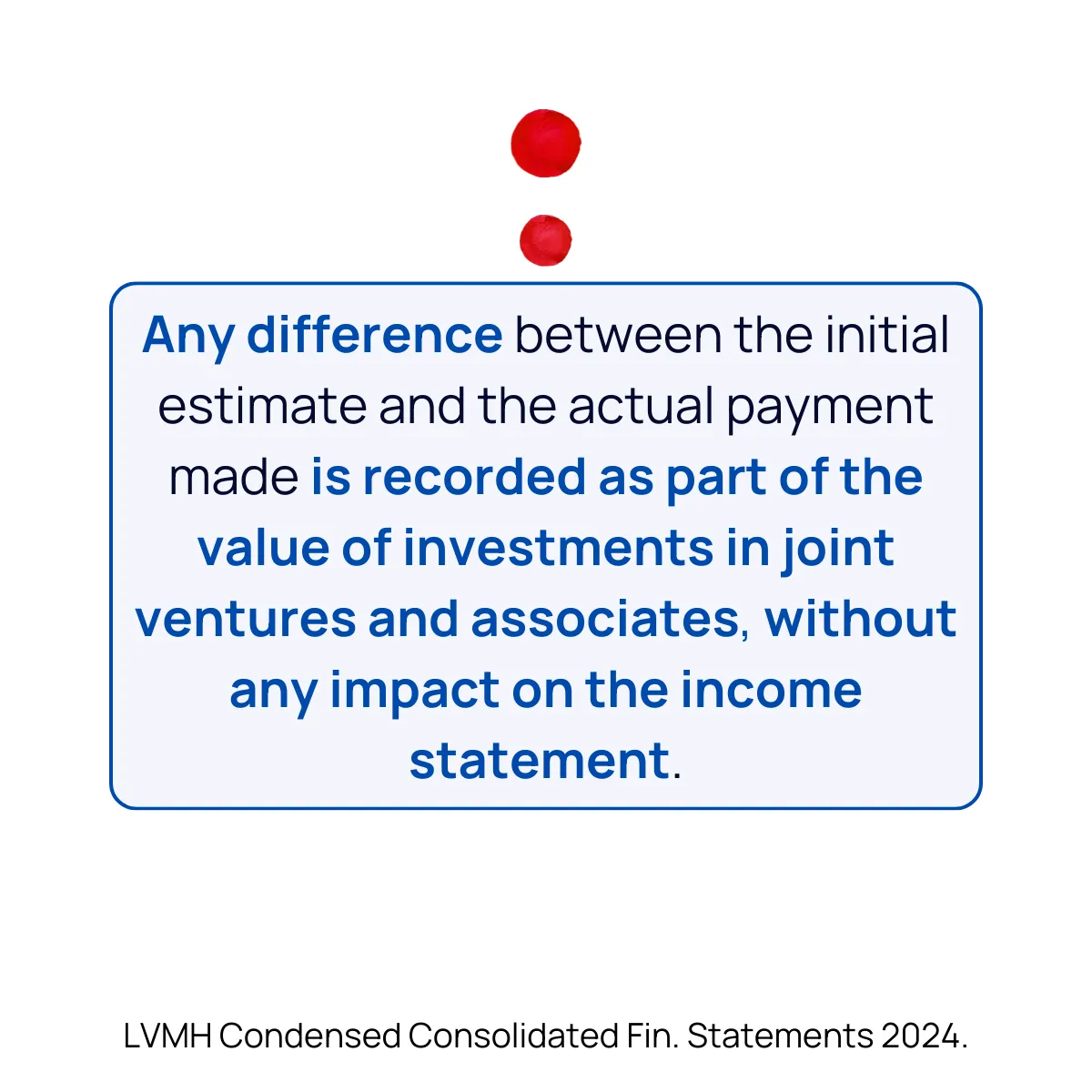

🔹Recognition of gains and losses from transactions with associates and joint ventures - upstream, downstream transactions,

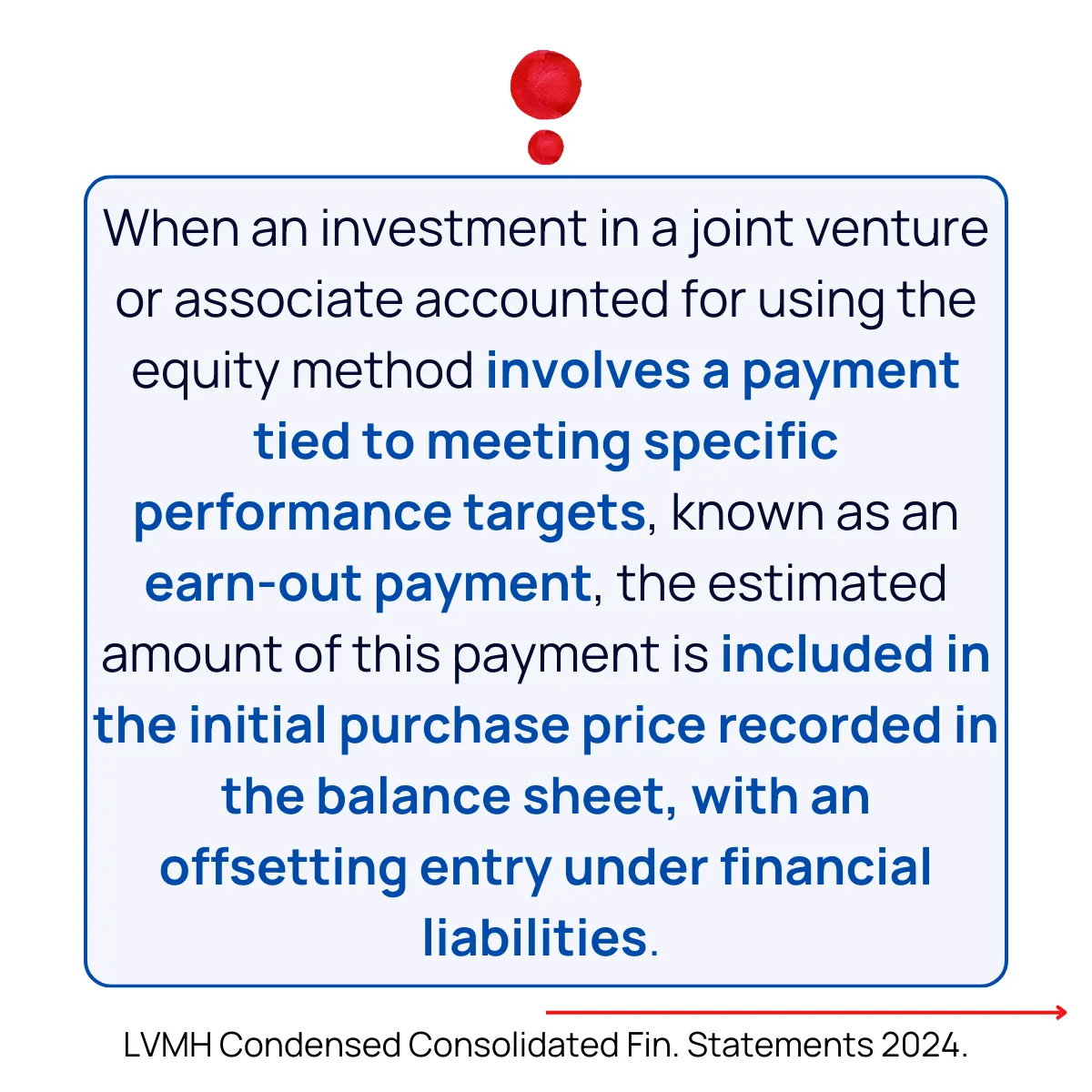

🔹Adding applciation questions concerning recognition of acquisition related costs when applying the equity method.

Link to the September IASB podcast discussing the latest updates:

https://lnkd.in/eGwaXBqy

📩 not yet subscribed to my newsletter?

Receive my bi-weekly accounting insights into your mailbox: https://lnkd.in/etKK5zvS

headline quote by Albert Einstein.