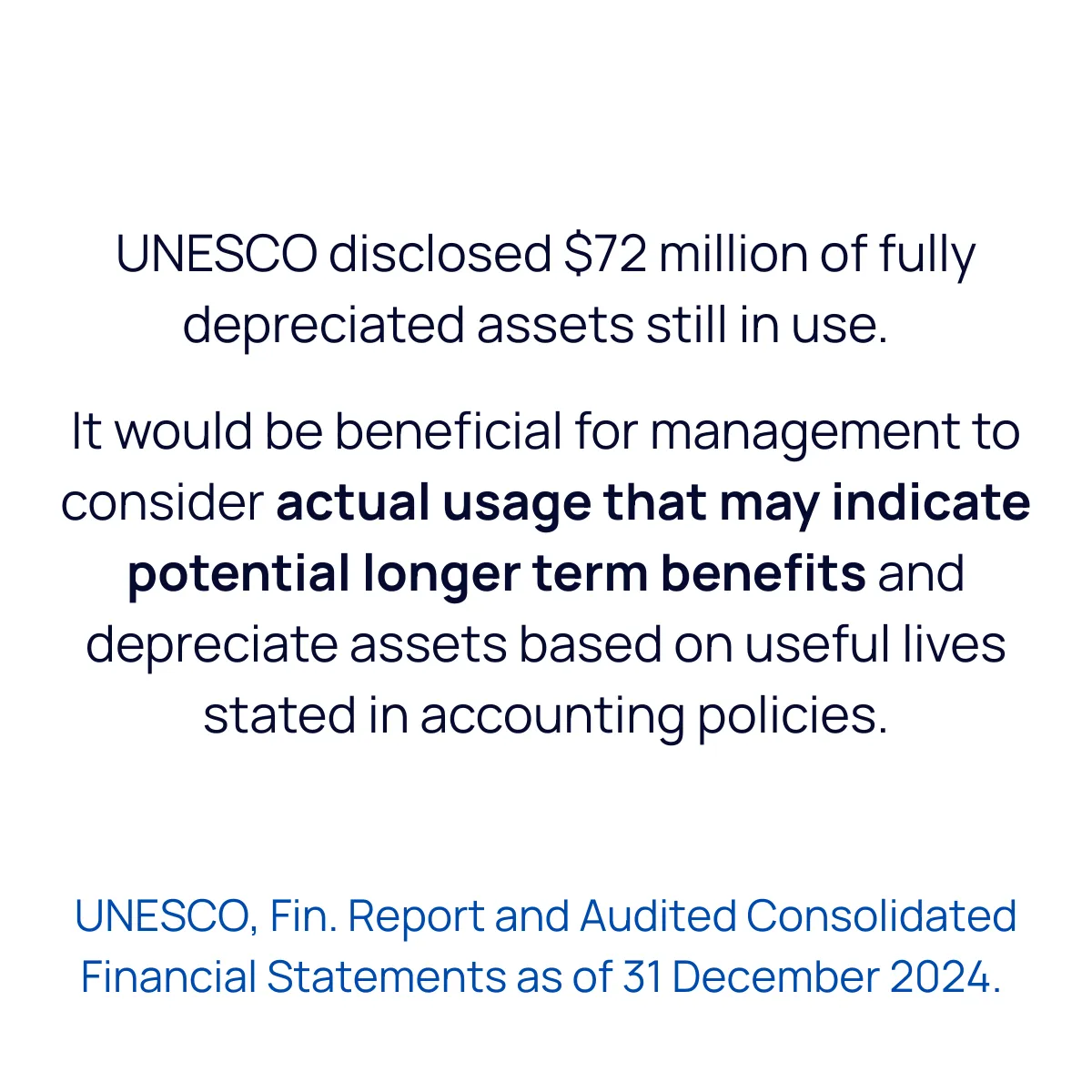

What actually are economic benefits?

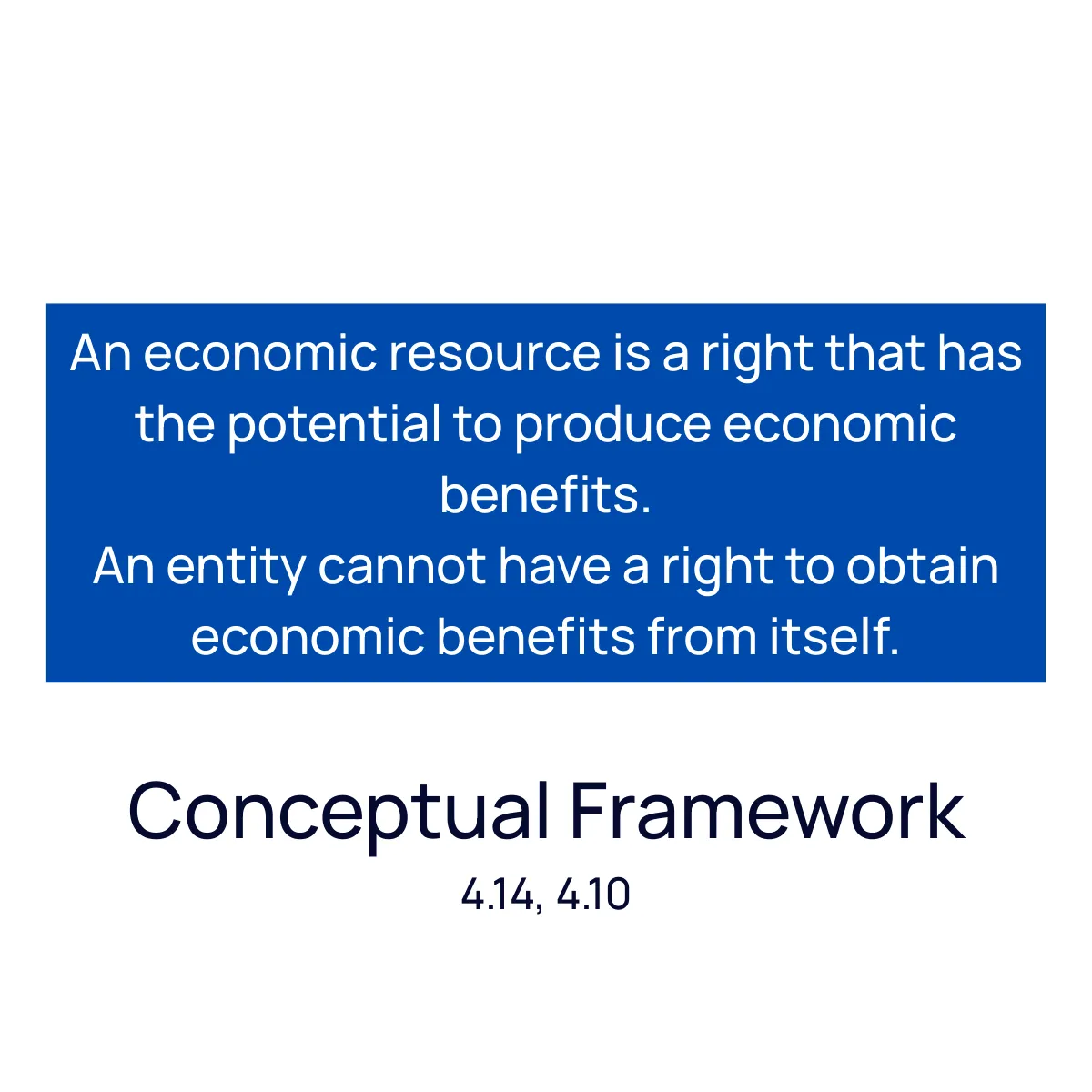

An economic resource is a right that has potential to produce economic benefits. An entity cannot have a right to obtain economic benefits from itself.

“Benefit for self and others, private and public interests are one and the same.”

The primary reason why businesses exist is to generate economic benefits.

Hardly any accounting concept must not be backed by the notion of economic resources/ benefits.

Notoriously known and (over-) used terms often suffer the loss of meaning.

What is the substance behind the two words (apart from the obvious ones - cash, revenue, return on investment)?

Paragraph 4.16 of the IFRS Conceptual Framework states:

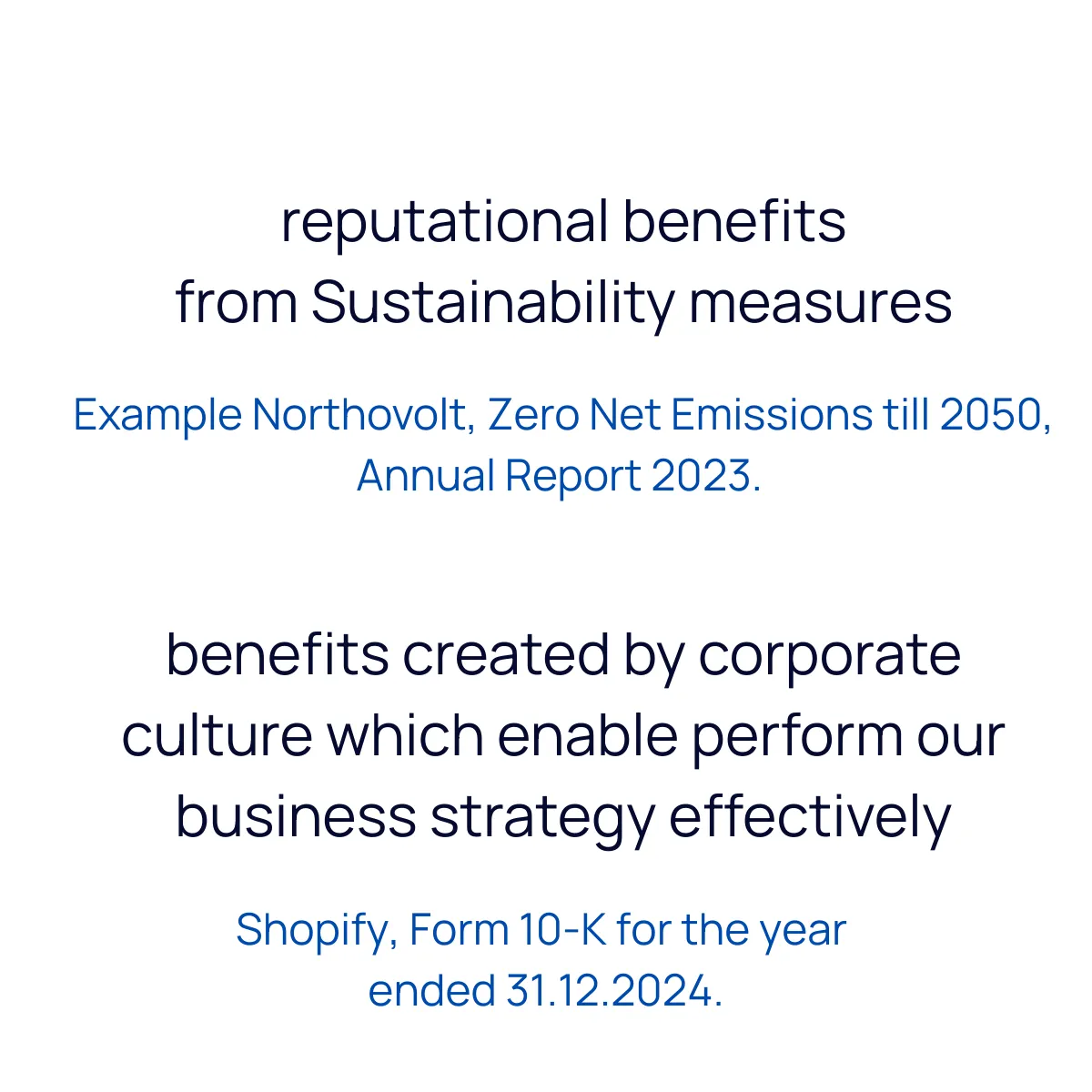

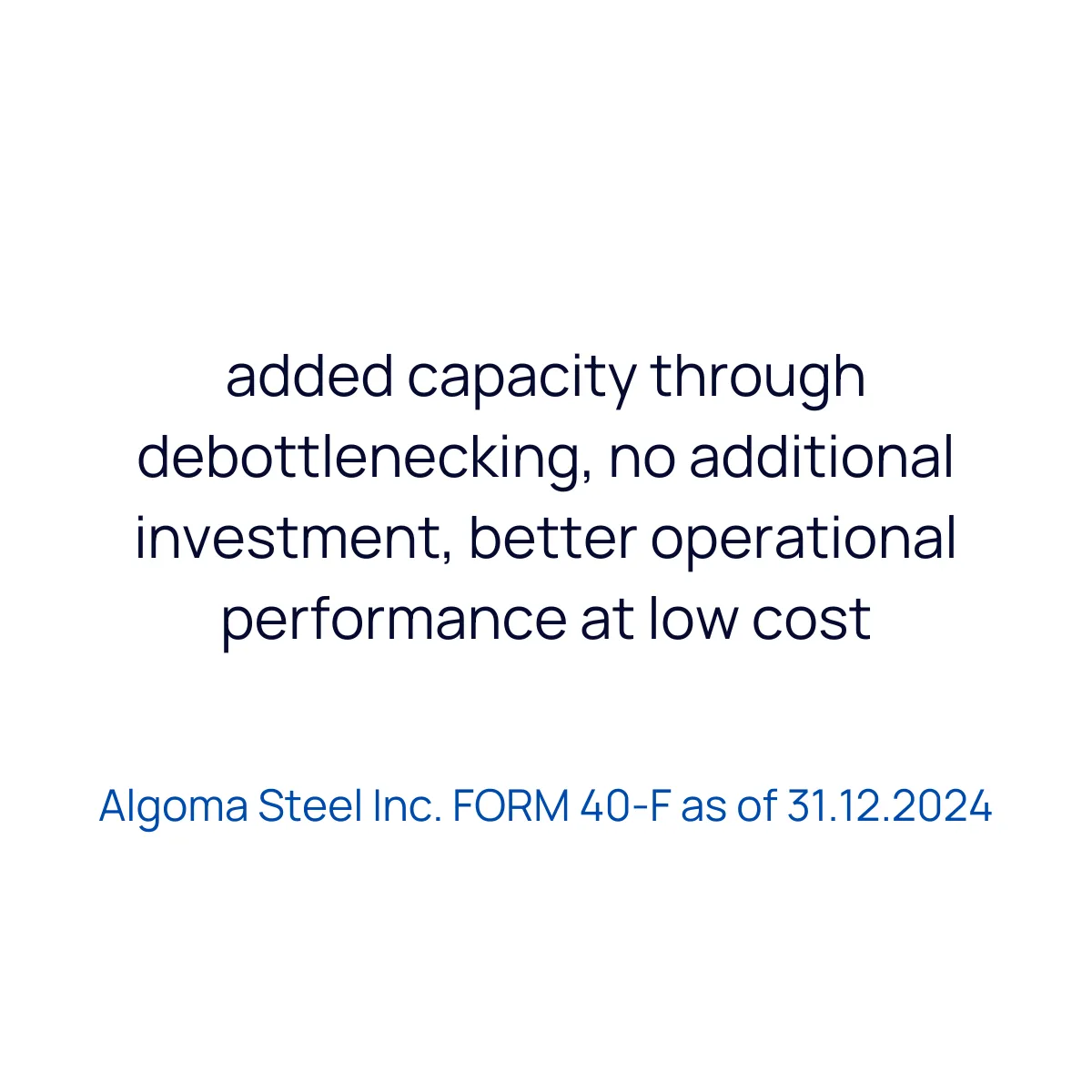

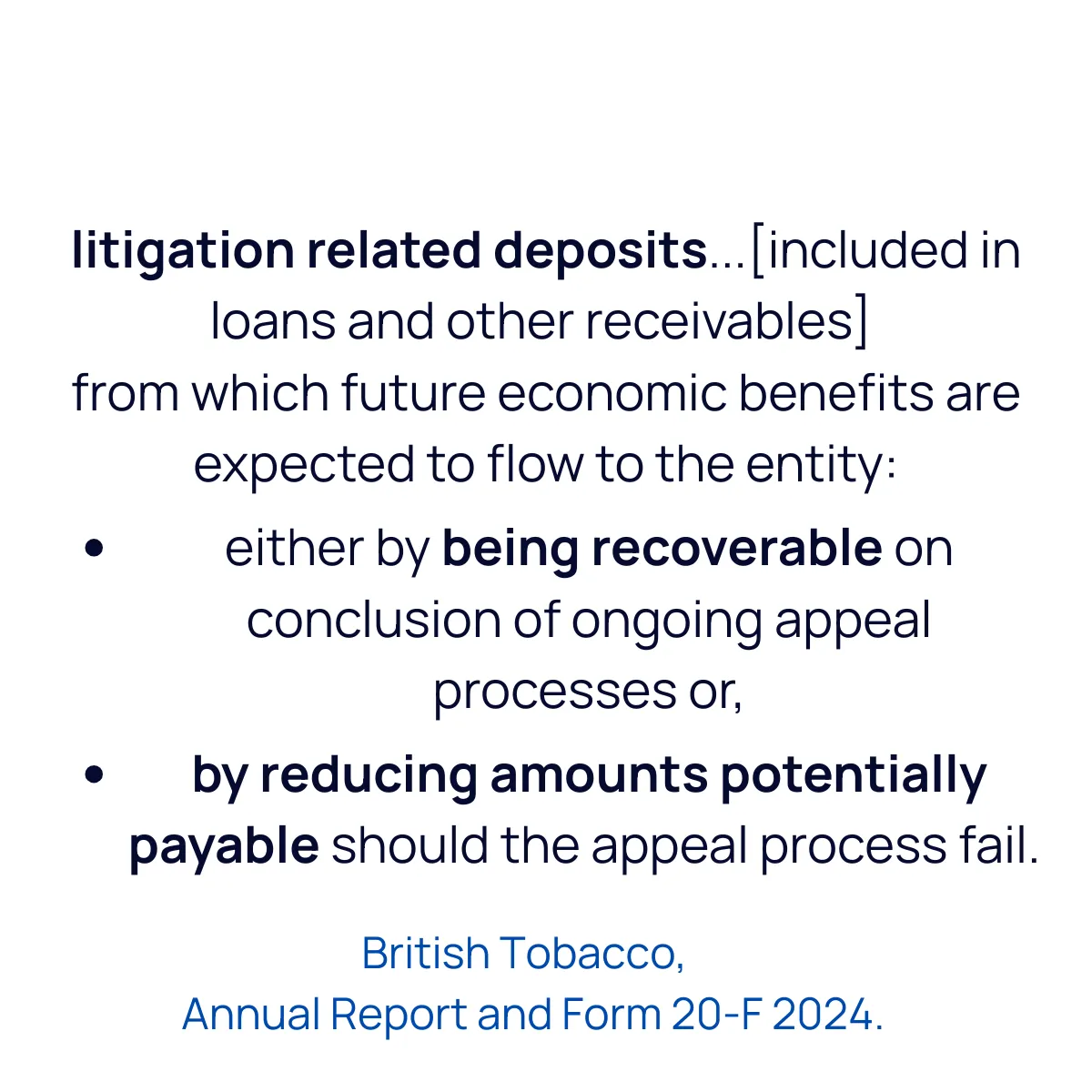

An economic resource could produce economic benefits for an entity by entitling or enabling it to do, for example, one or more of the following:

a) receive contractual cash flows or another economic resource;

b) produce cash inflows or avoid cash outflows by, for example:

- using the economic resource either individually or in combination with other economic resources to produce goods or provide services;

- using the economic resource to enhance the value of other economic resources; or

- leasing the economic resource to another party;

d) receive cash or other economic resources by selling the economic resource; or

e) extinguish liabilities by transferring the economic resource.

This post is meant to showcase some examples and hopefully start a discussion. See the attached carousel.

headline quote conveys the business philosophy of Sumimoto Corporation, Japan.