Back to Basics: Double Entries

With an understanding of double-entry principles, the solution becomes evident.

I knew a guy in my old days at Big 4, let’s call him John. John was famous in and around the office by repeating these two “rules” to anyone willing to listen:

Stop messing around at your computers. Go and talk to people - that's how you do an audit!

I don't need to know double entries. I am making a “qualified guess”!

John was a partner at that audit firm.

Even after all these years, I have fond memories of John. And while I can relate to his first quote, I'm quite radical about the second one.

When you're studying accounting or fresh out of an audit qualification, you can probably pull any accounting entry off your sleeve.

But later, as you climb the career ladder and take on broader responsibilities, the nitty-gritty of accounting entries tends to fade into the background.

My point is: double entries can be your golden thread.

They guide you through endless management discussions, help you solve complex issues, and provide quick answers when your forecasts don't match actuals or when you're desperately searching for ways to save resources.

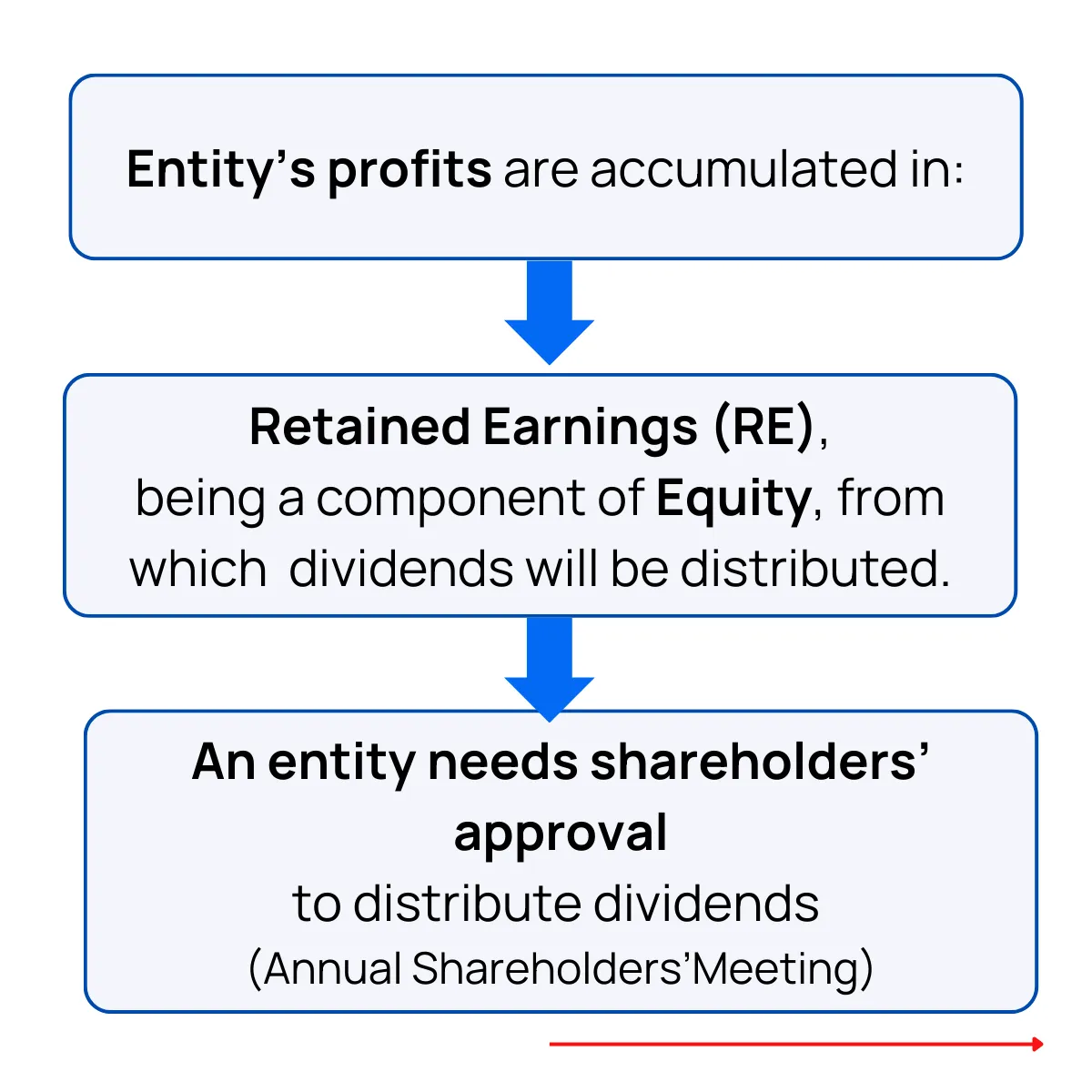

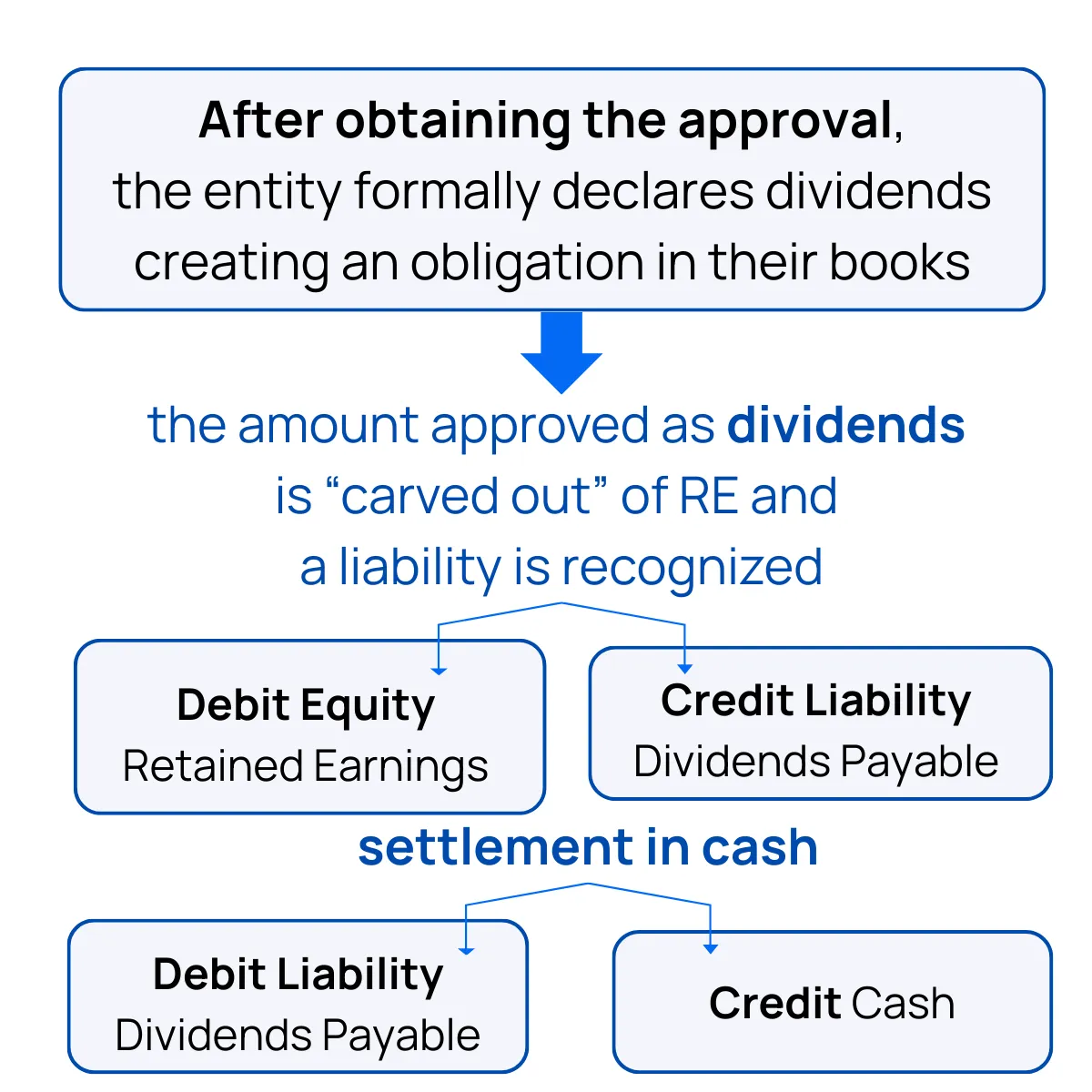

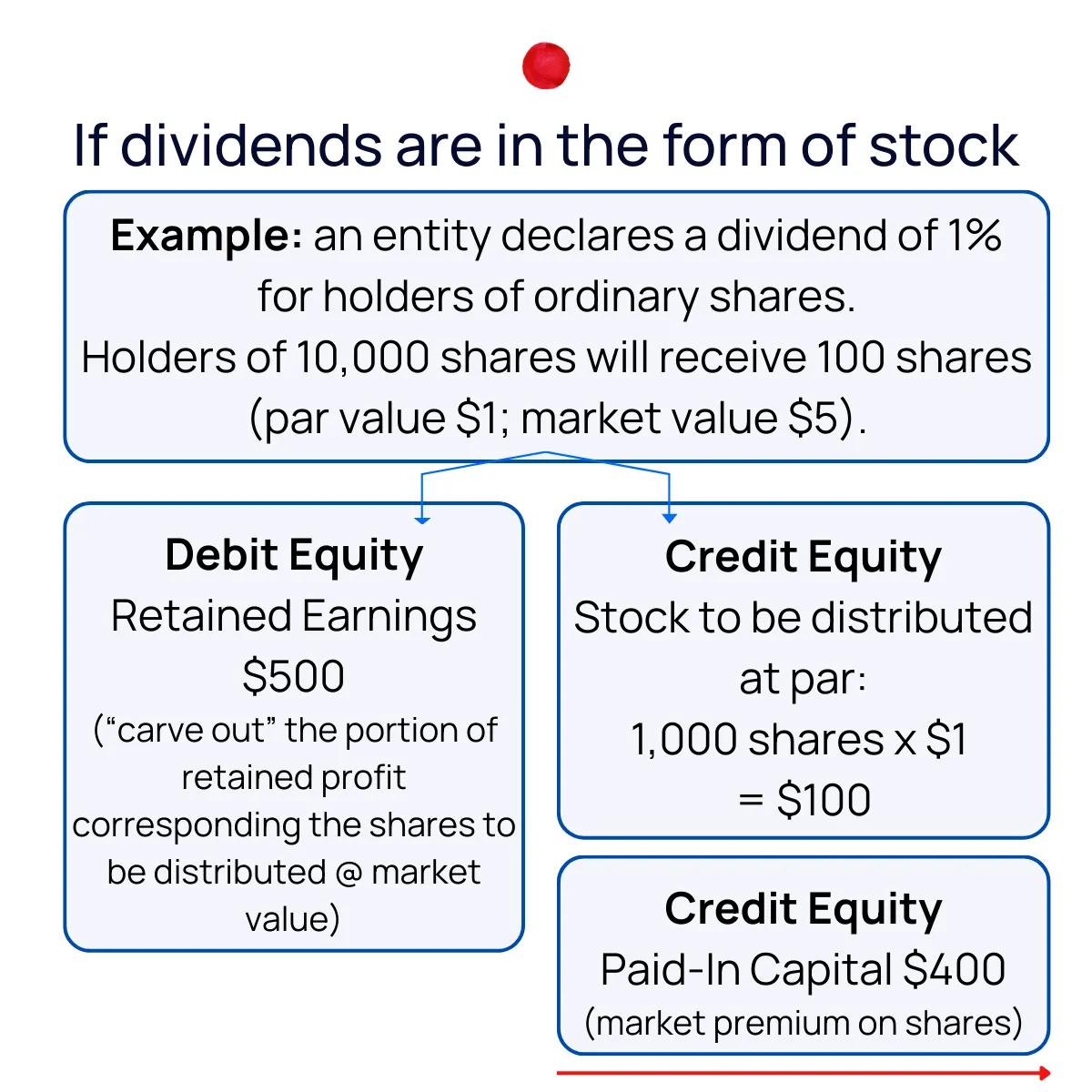

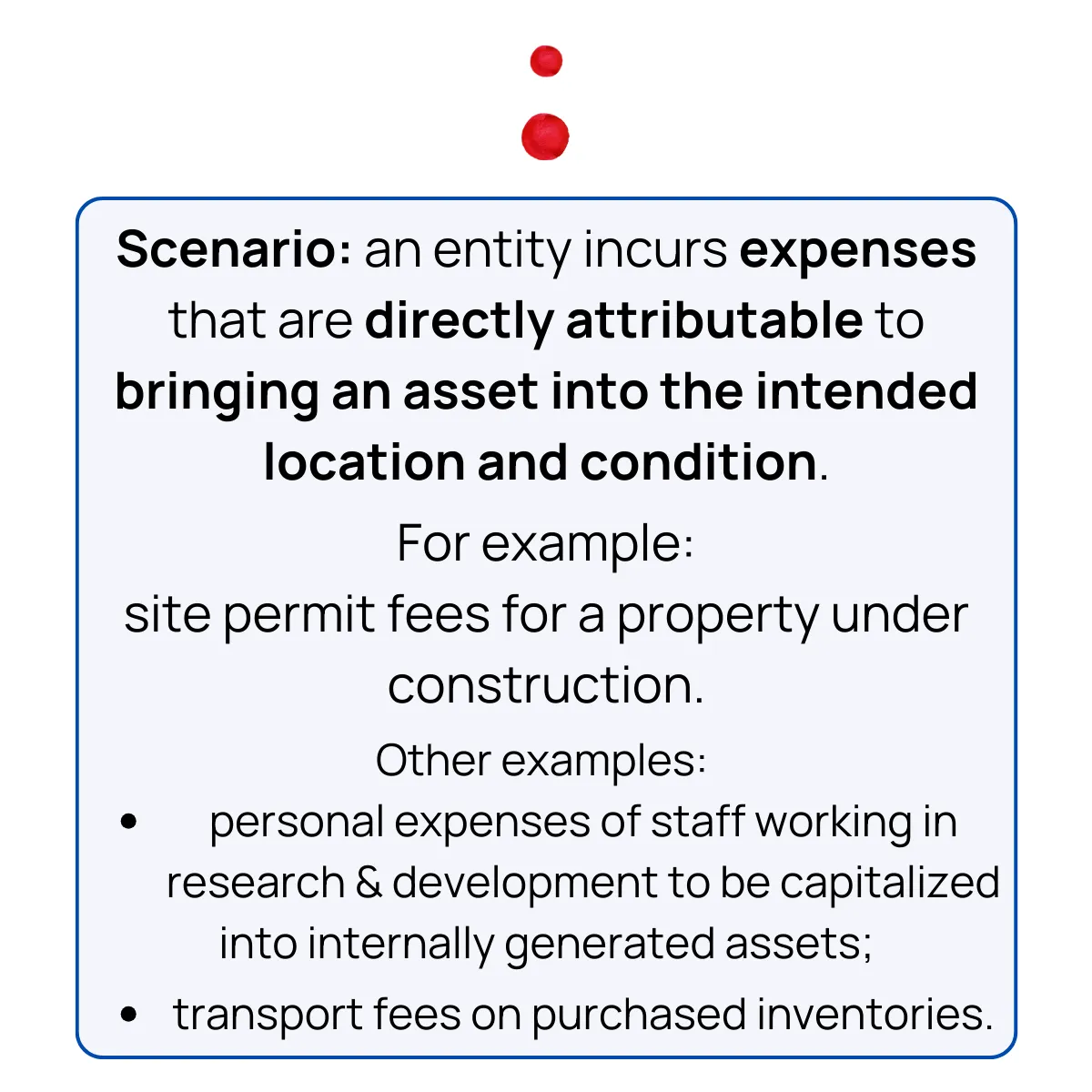

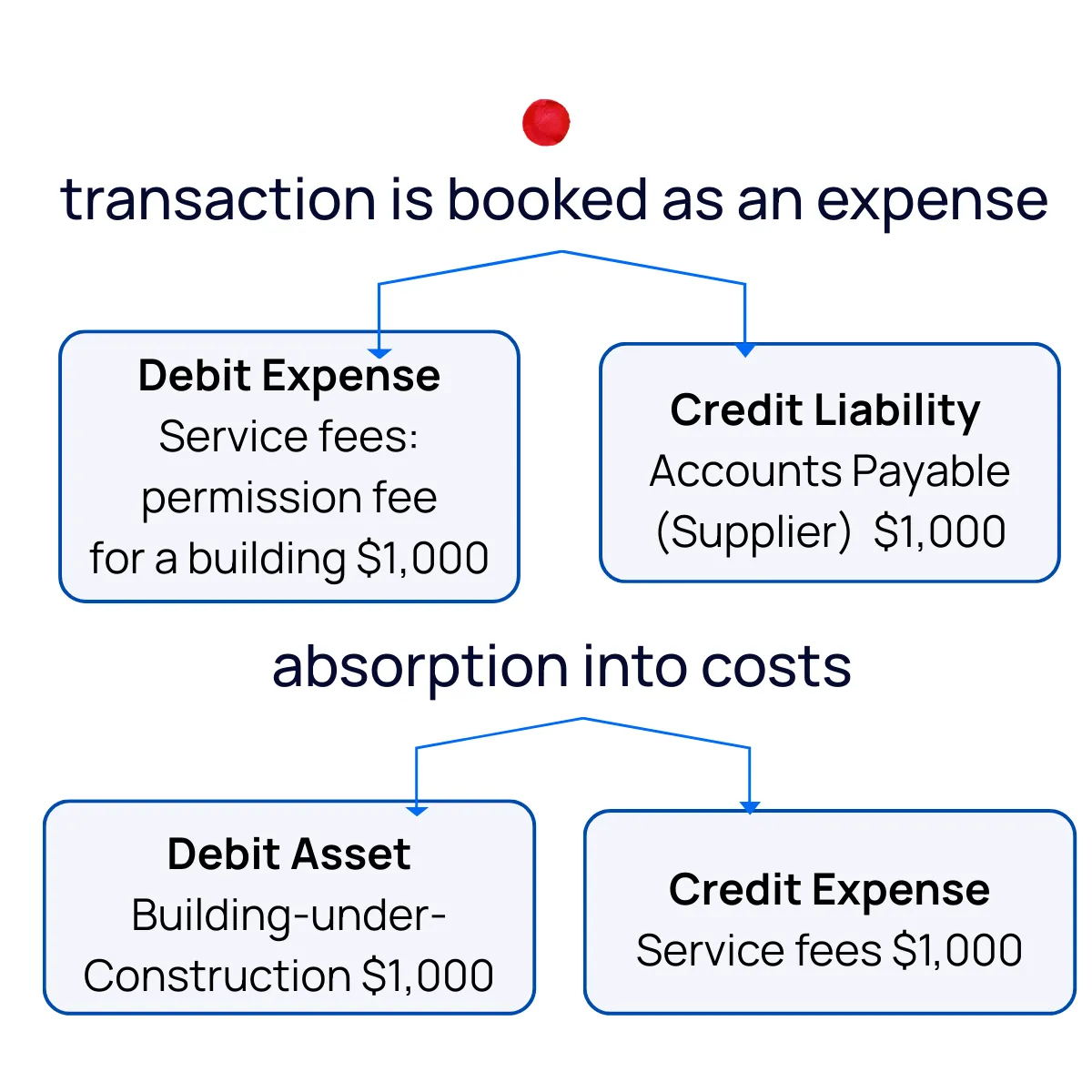

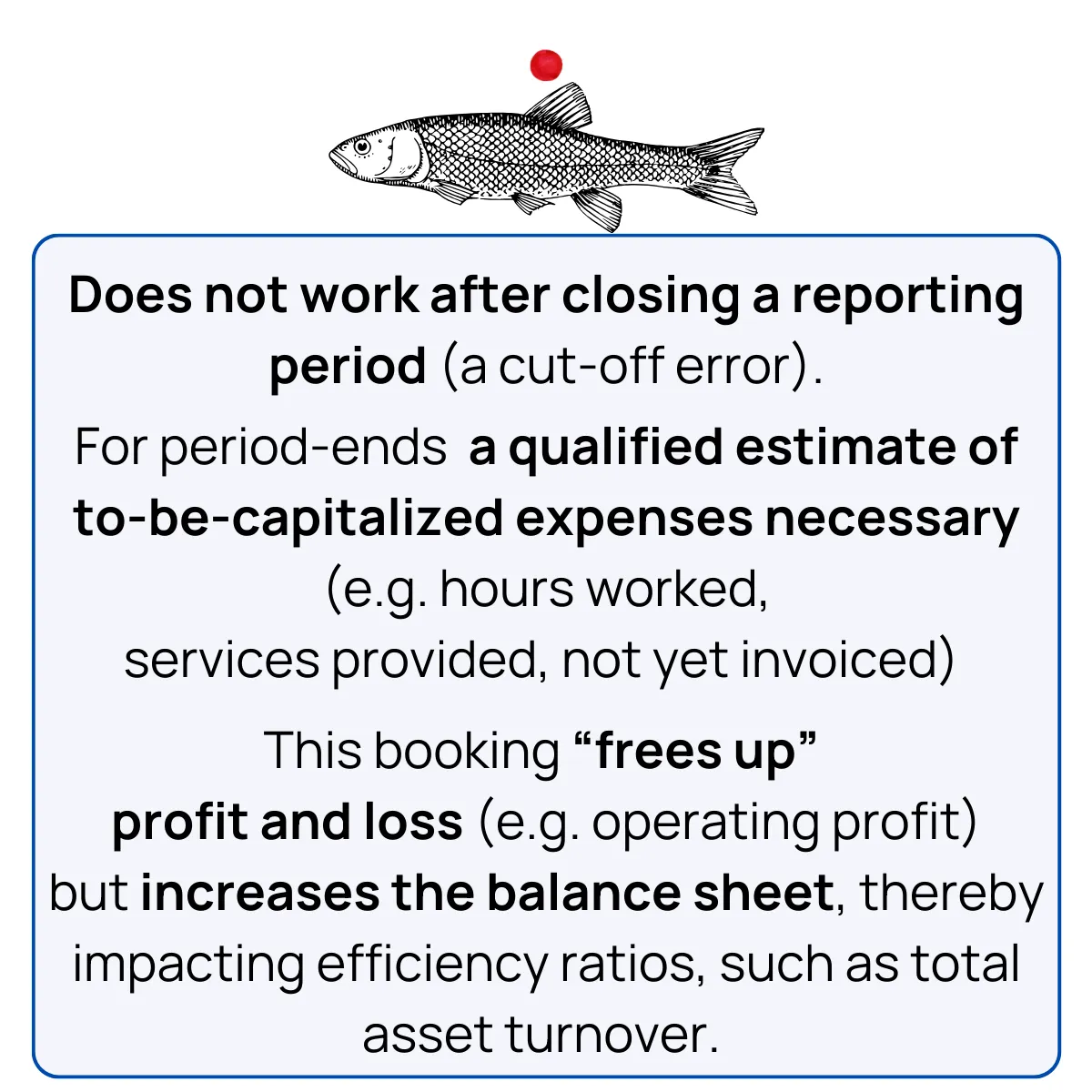

⏩ In today' post I am sharing two examples of booking entries I came across recently - distribution of dividends and absorption of expenses into the cost of an asset plus some practical thoughts to help you see the big picture.