IFRS 18 is not about labels

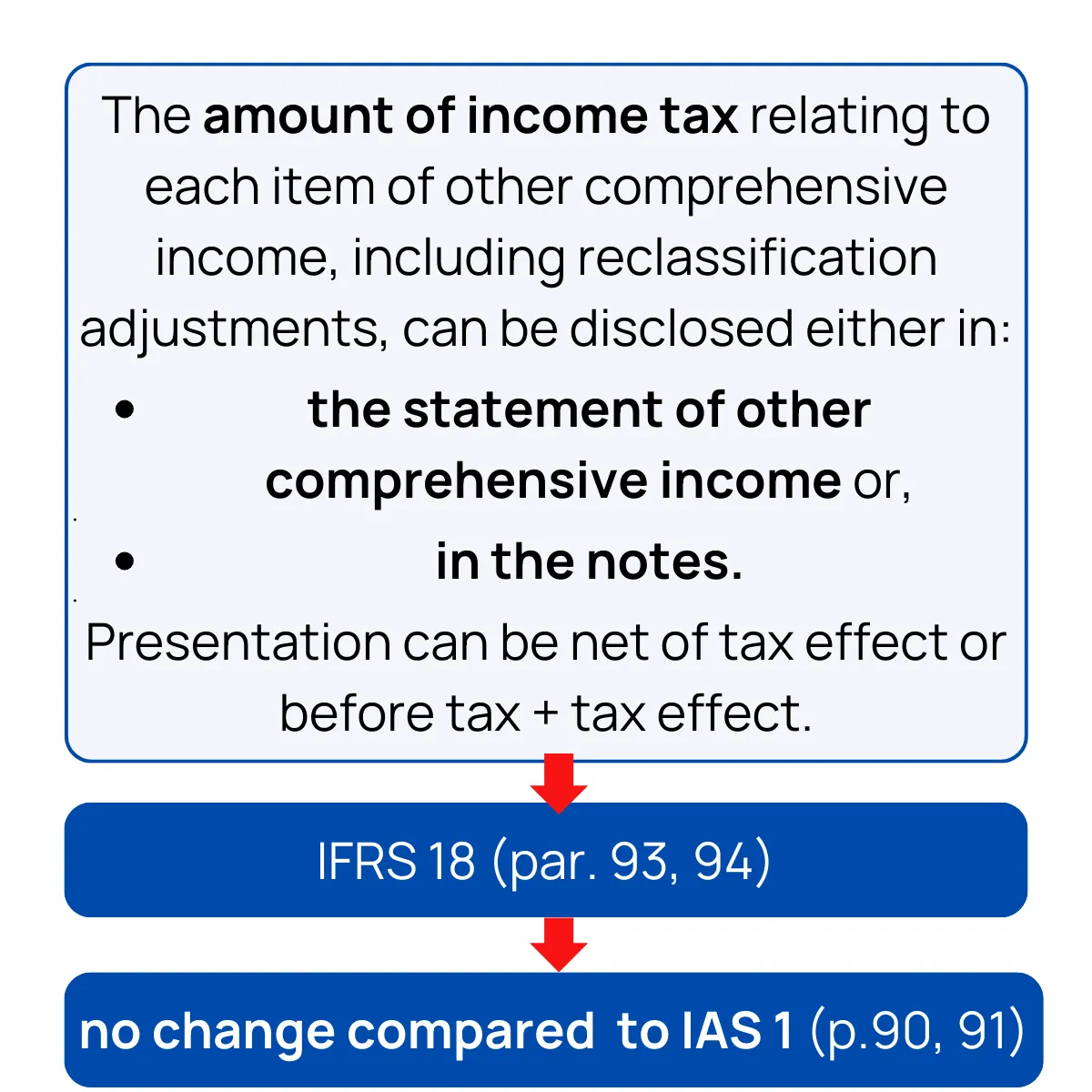

How to treat items of Other Comprehensive Income in the financial statements prepared in accordance with IFRS?

"We were thinking of hiring someone who is also a mother for the first time." -"We look for an Eastern European woman for our corporate talent program."

These sentences were said - independently of each other - by two good-hearted men, at two separate occasions I applied for an opportunity.

Getting to know them and working with them later, I became absolutely certain, that they did not want me to feel uncomfortable.

It was simply the way these men tried to talk to, include and encourage a person, which was different from “the standard.”

I received both opportunities and loved the time spent there.

And years later I still ask myself whether I got the chances because of my skills...or because of the “labels”.

IFRS 18 Presentation and Disclosure in Financial Statements is perceived by many as a "label" exercise.

Classify, categorize, put the right label on.

In my opinion, it is quite the opposite.

Look at the core of your business and forget for a moment those categories (operating, investing, financing, income tax and discontinued operations).

IFRS 18 is a chance to look below the dusty labels and discover what actually matters.

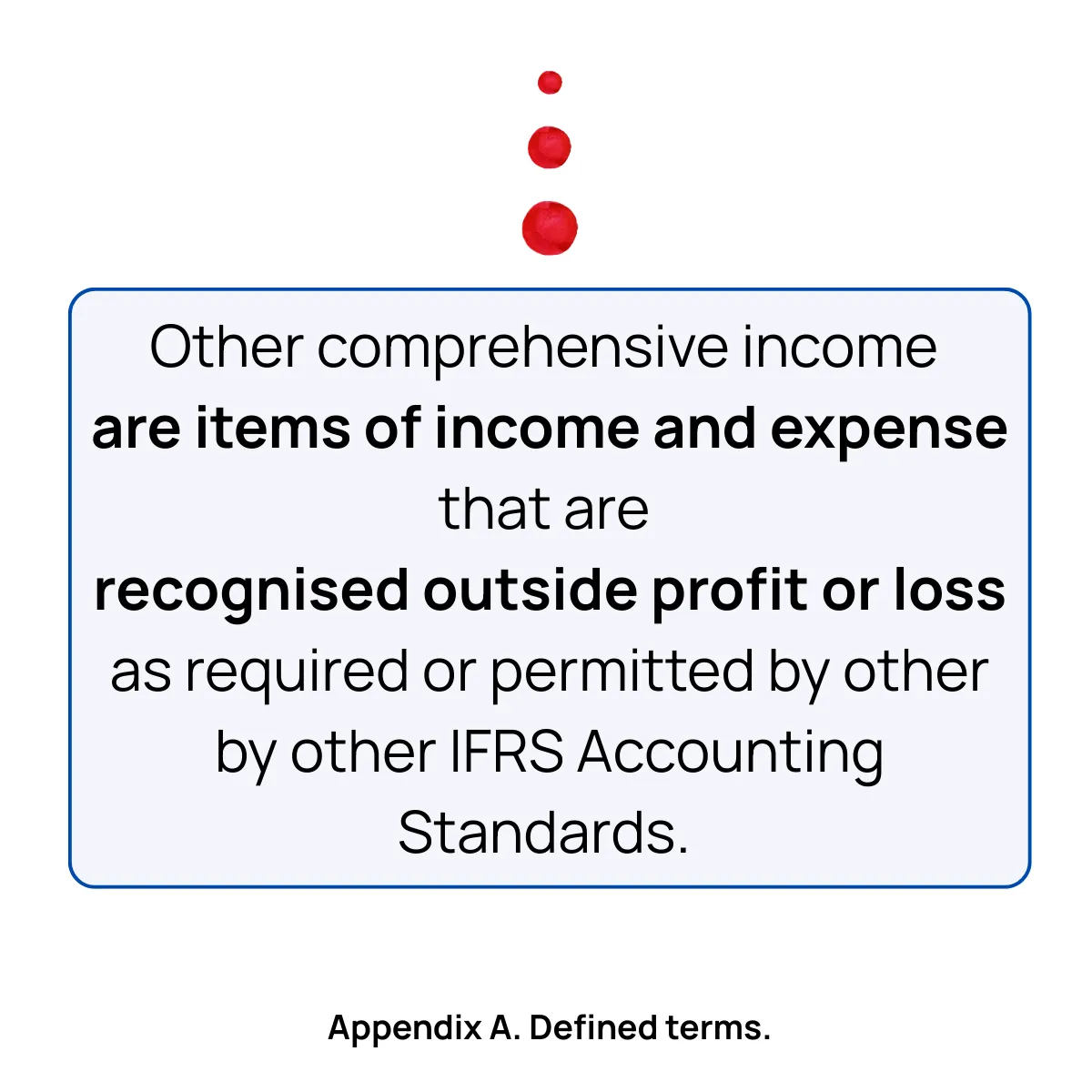

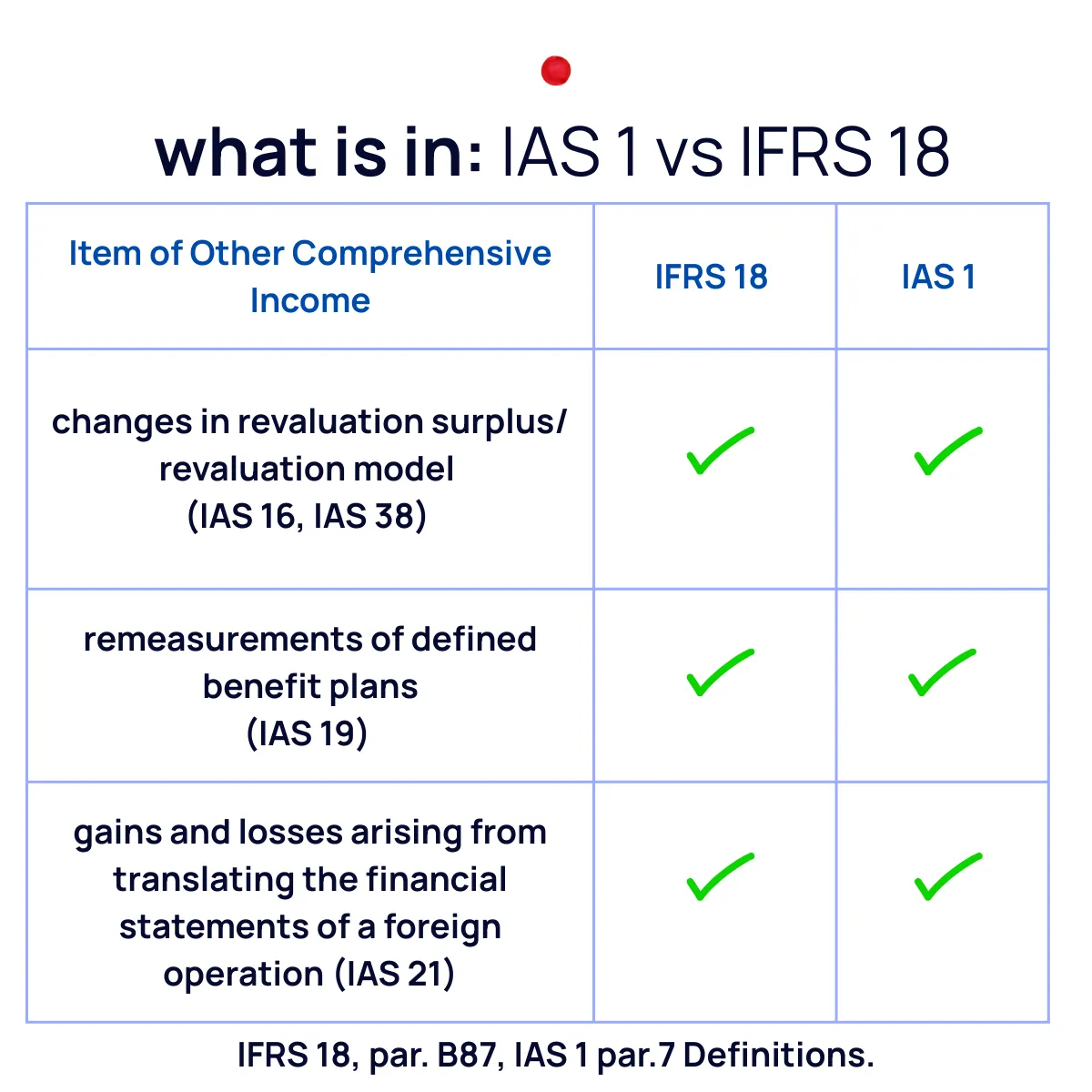

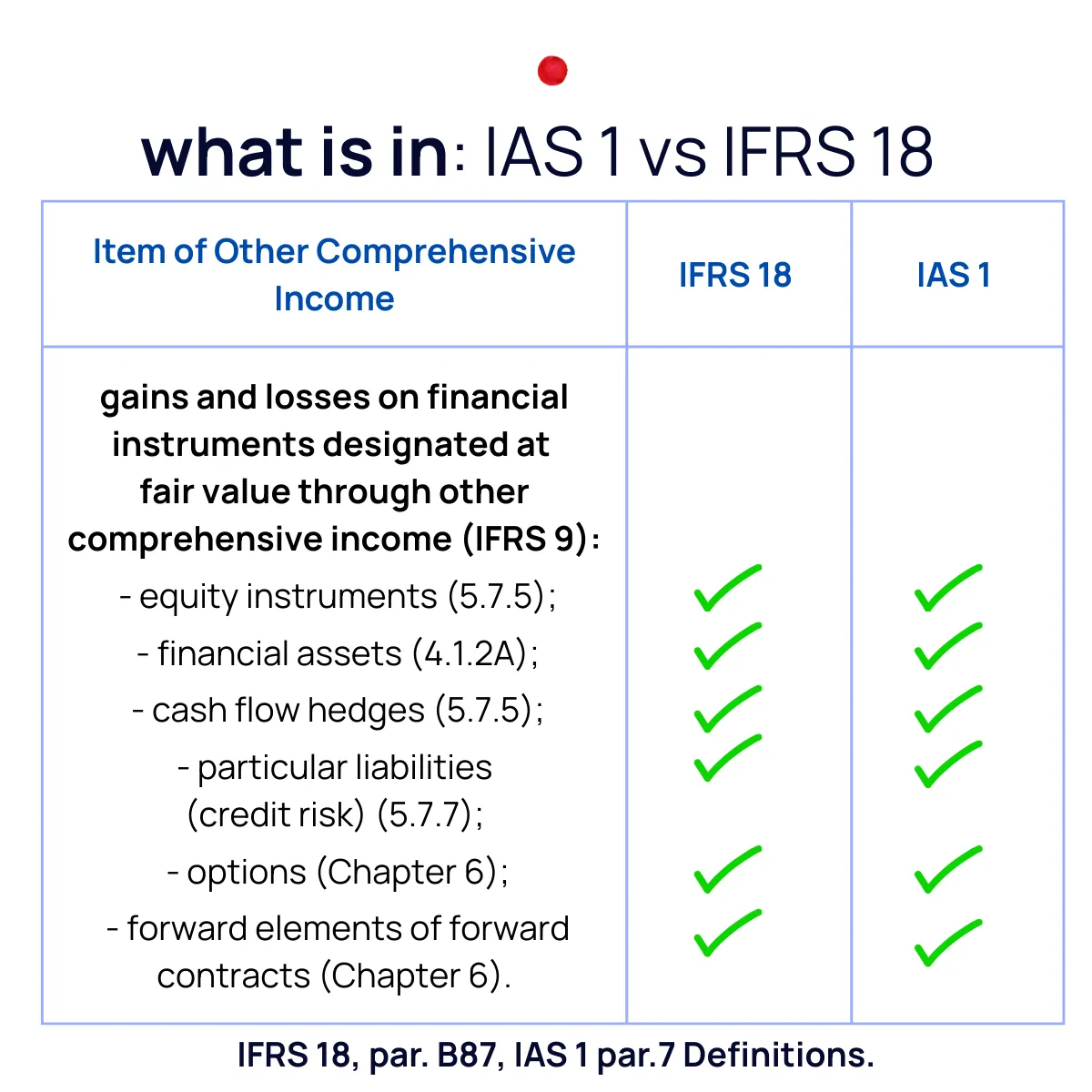

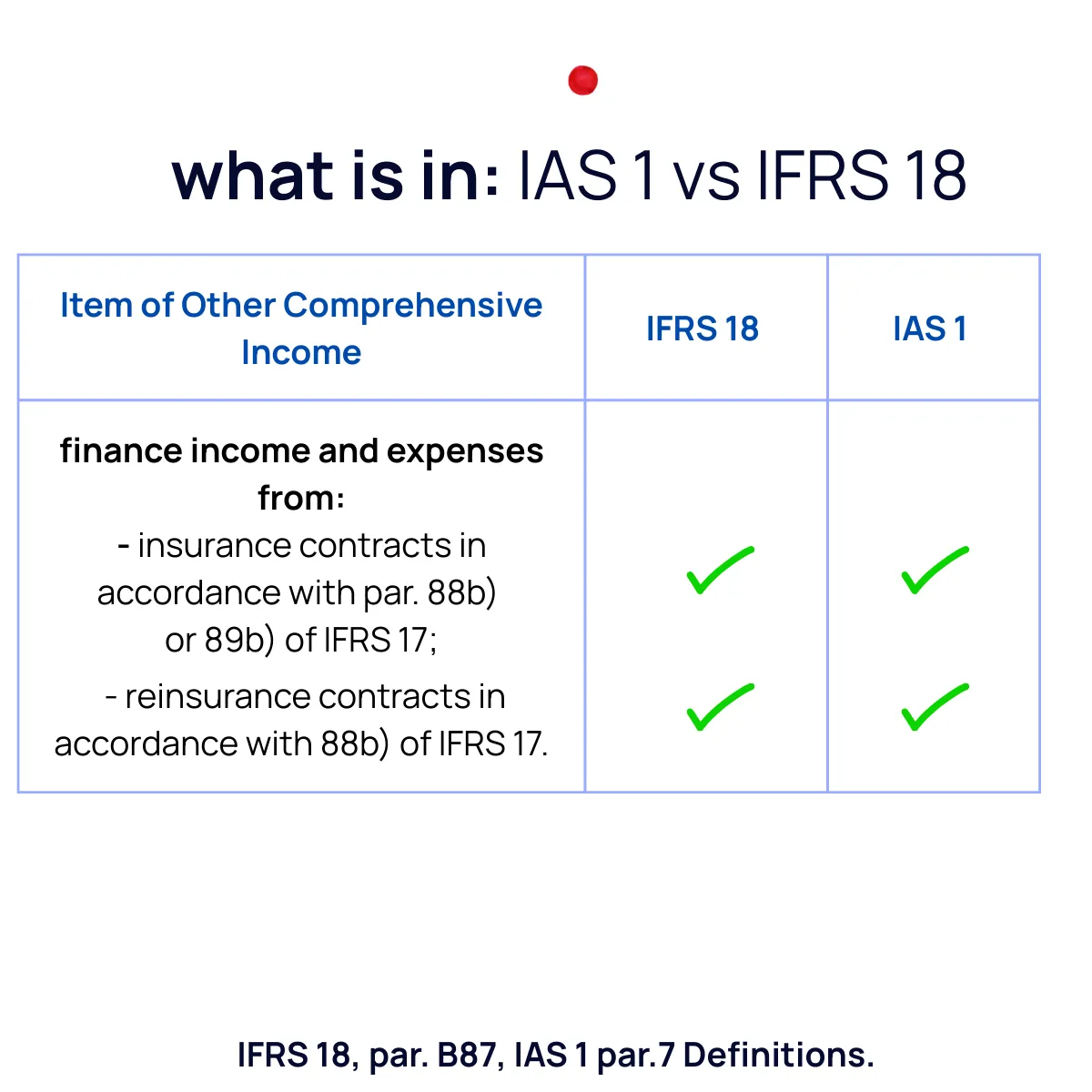

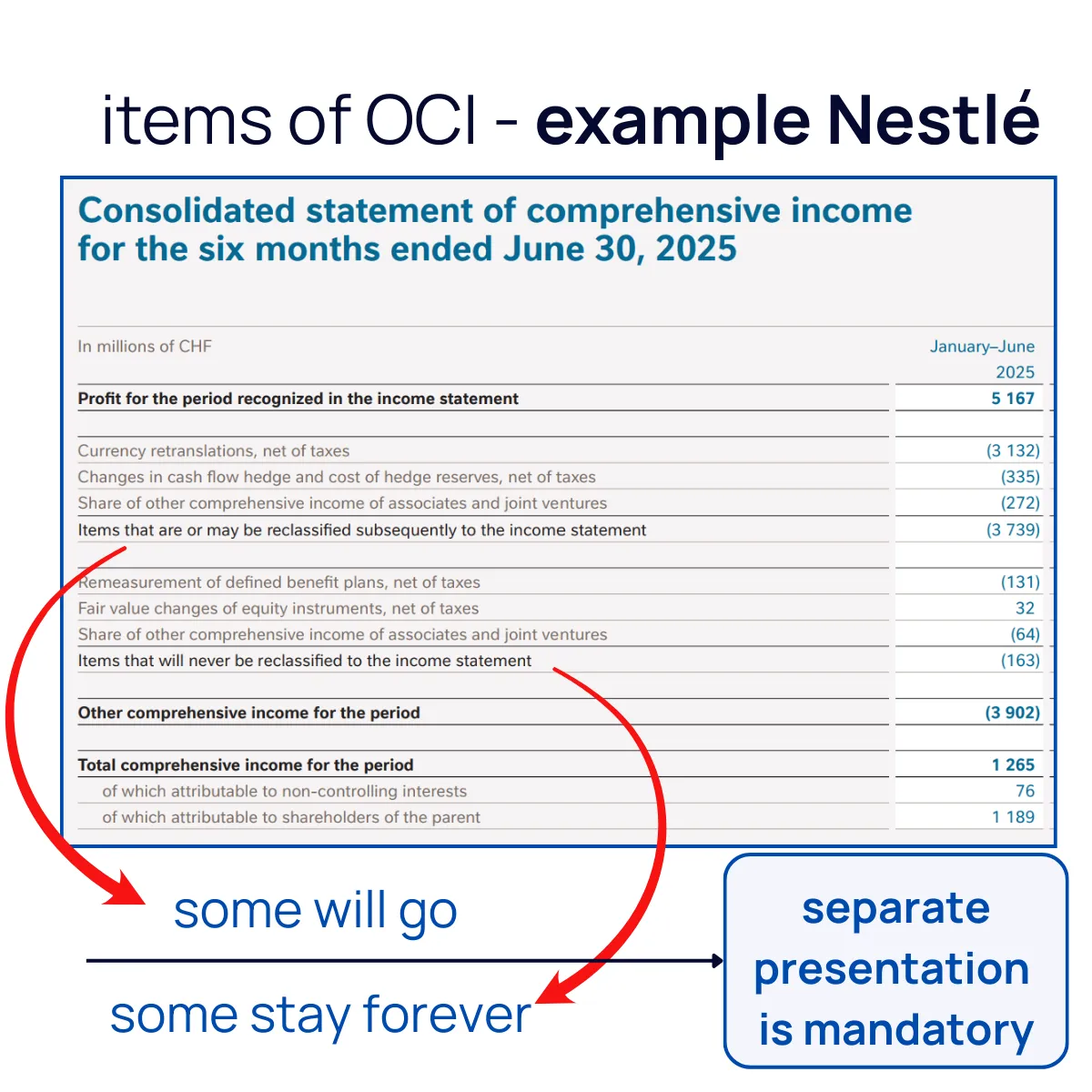

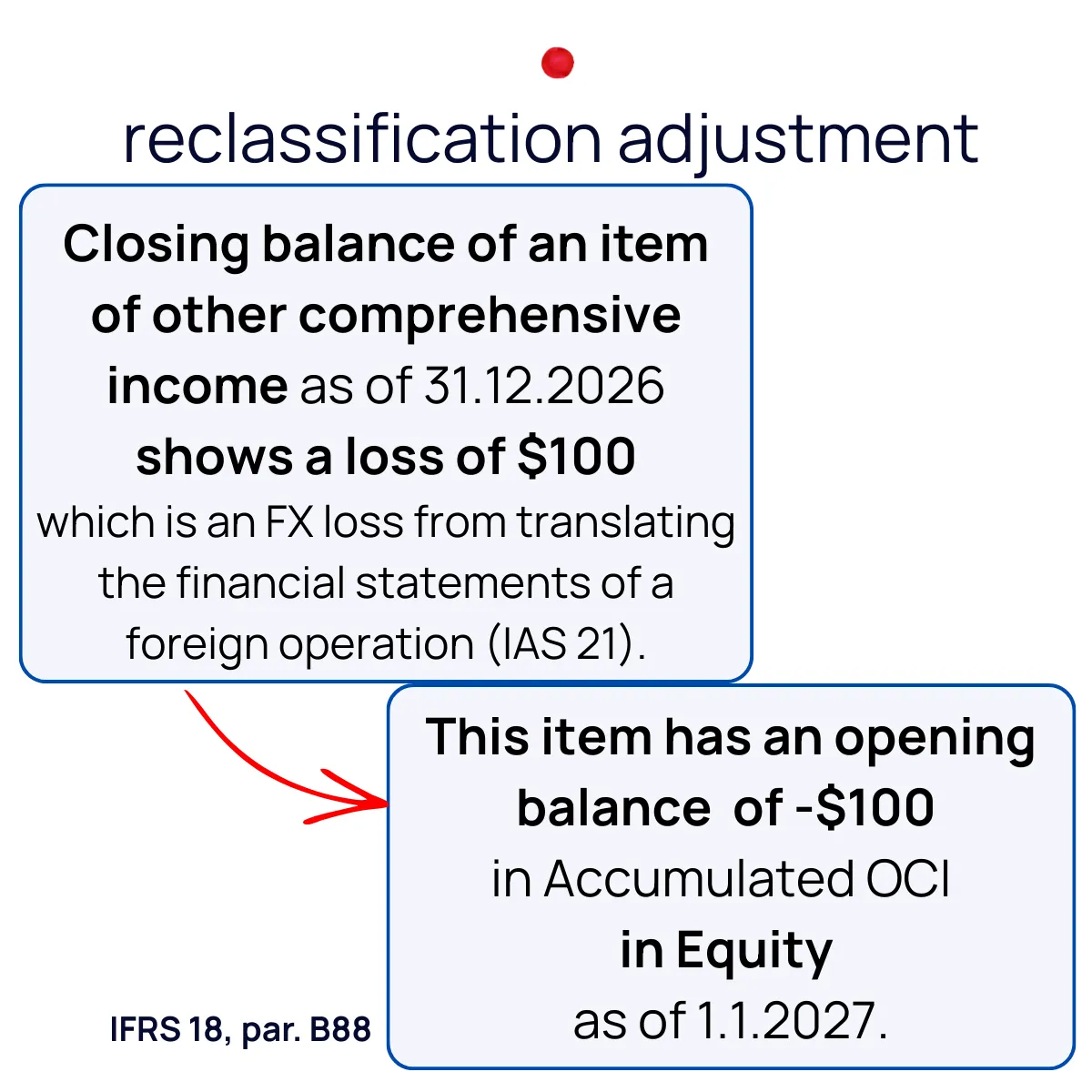

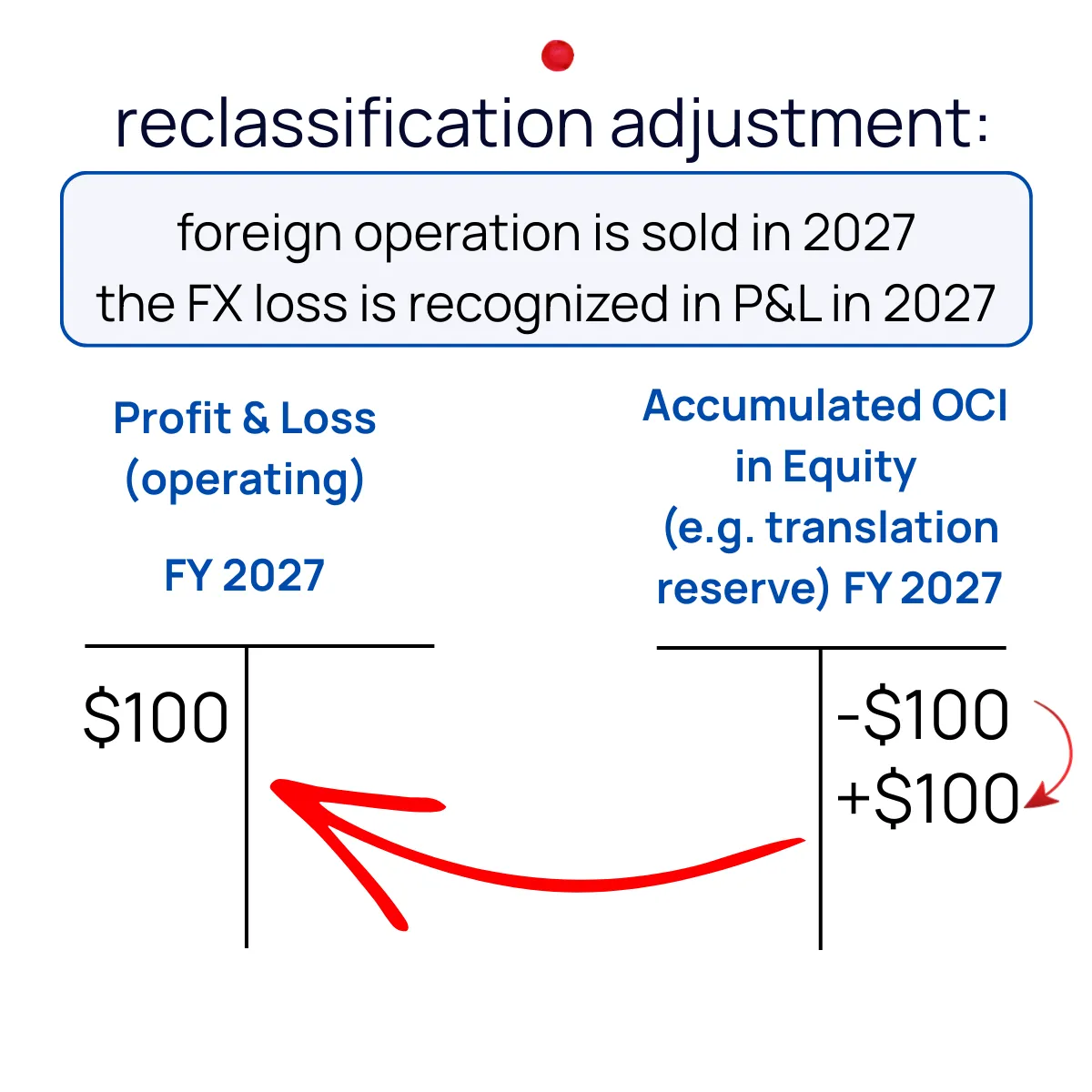

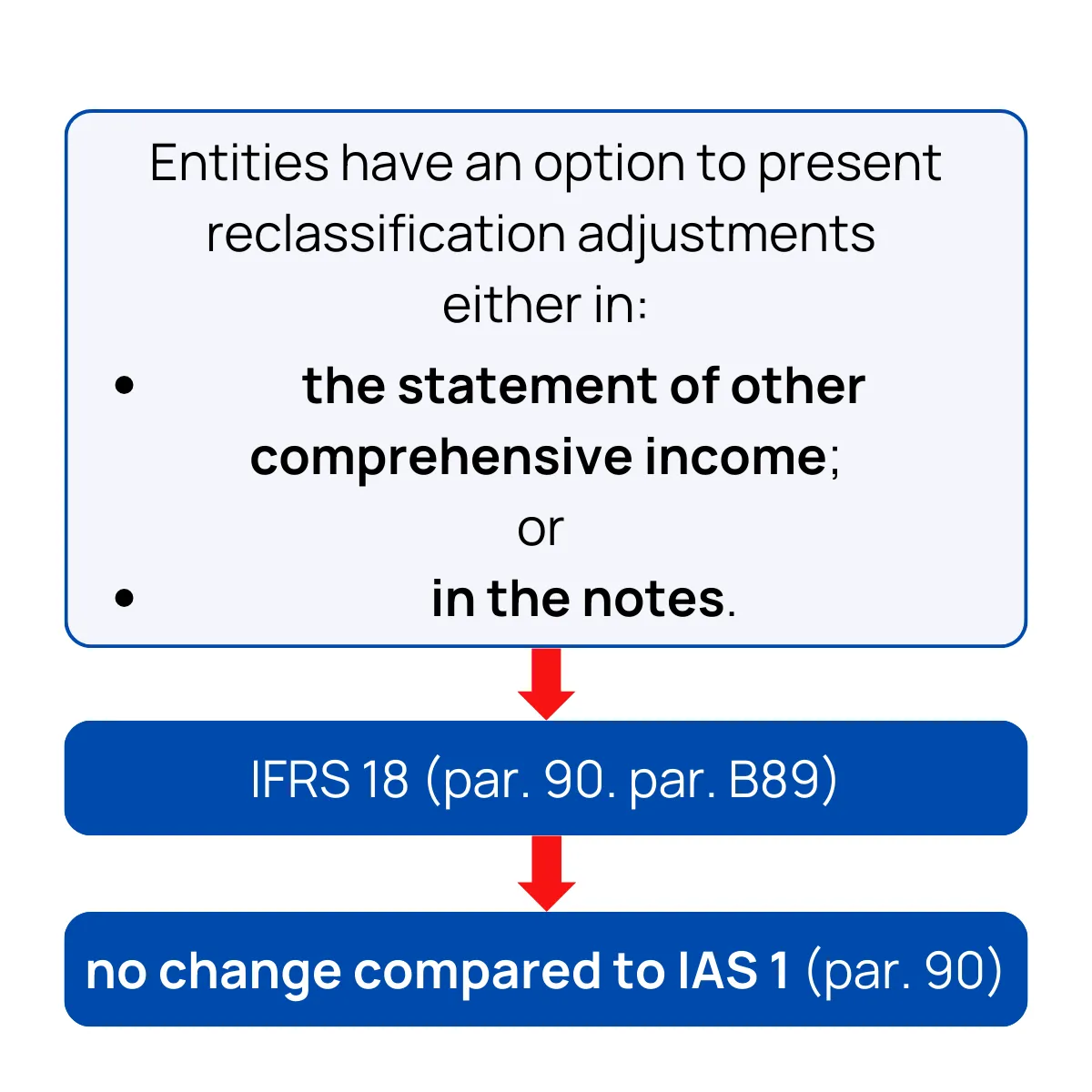

⏩ Todays carousel is about Other Comprehensive Income in accordance with the IFRS 18, in a nutshell.