Off-Balance Sheet Accounting

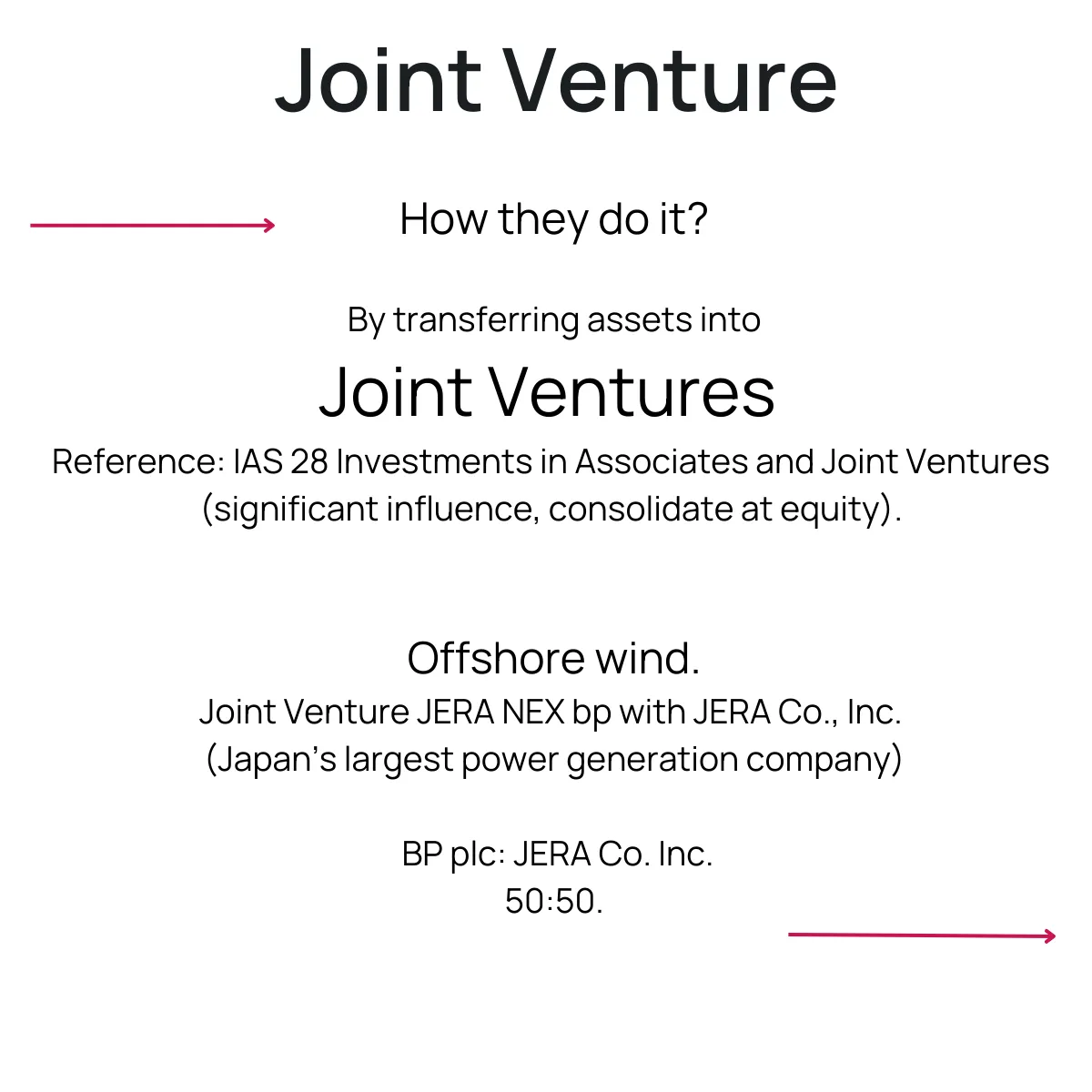

Companies transfer assets into Joint Ventures.

Off-Balance Sheet Accounting.

“Sometimes the best hiding place is the one that`s in plain sight”. Stephanie Meyer.

In my compilation of "Top Ten task for your accountant" this one occupies the highest bars:

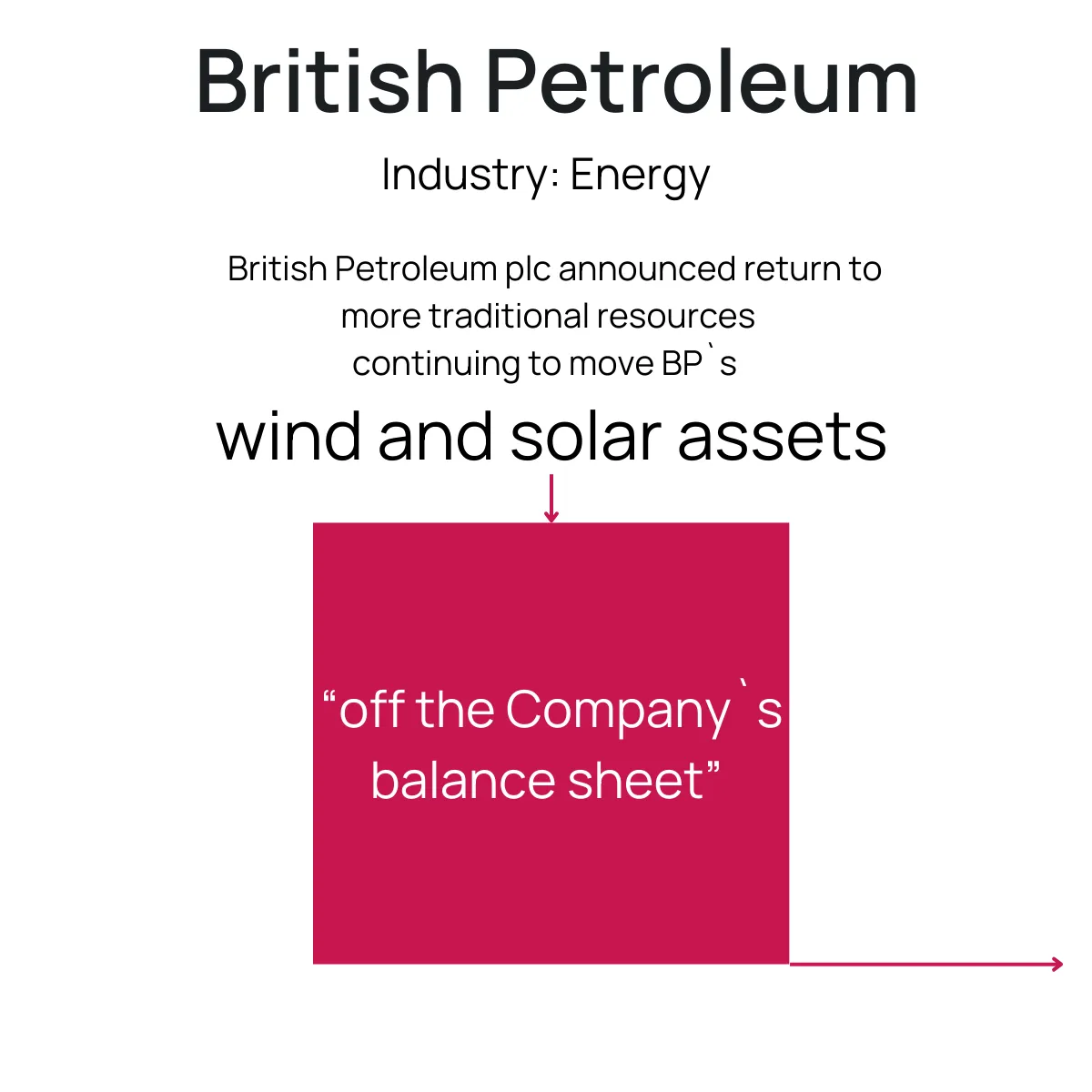

“We need to have those assets off the balance sheet."*

and there is no option B. to that

Remember the famous quote by Sir David Tweedie dating back to 'before-IFRS 16-era'?

“One of my greatest ambitions before I die is to fly in an aircraft that is on an airline`s balance sheet.”

Airlines (and others) largely structured their lease arrangements in a way that allowed them to be accounted for as a service (“operating lease”, IAS 17) and thus avoided assets and corresponding liabilities “on the balance sheet.”

The effect analysis of the IASB assessed ca. $1.25 trillion of “non-cancellable future cash obligations committed under operating leases and not recognized on balance sheets.”

The off-balance sheet treatment used to be (and still is!) popular for understandable rationale:

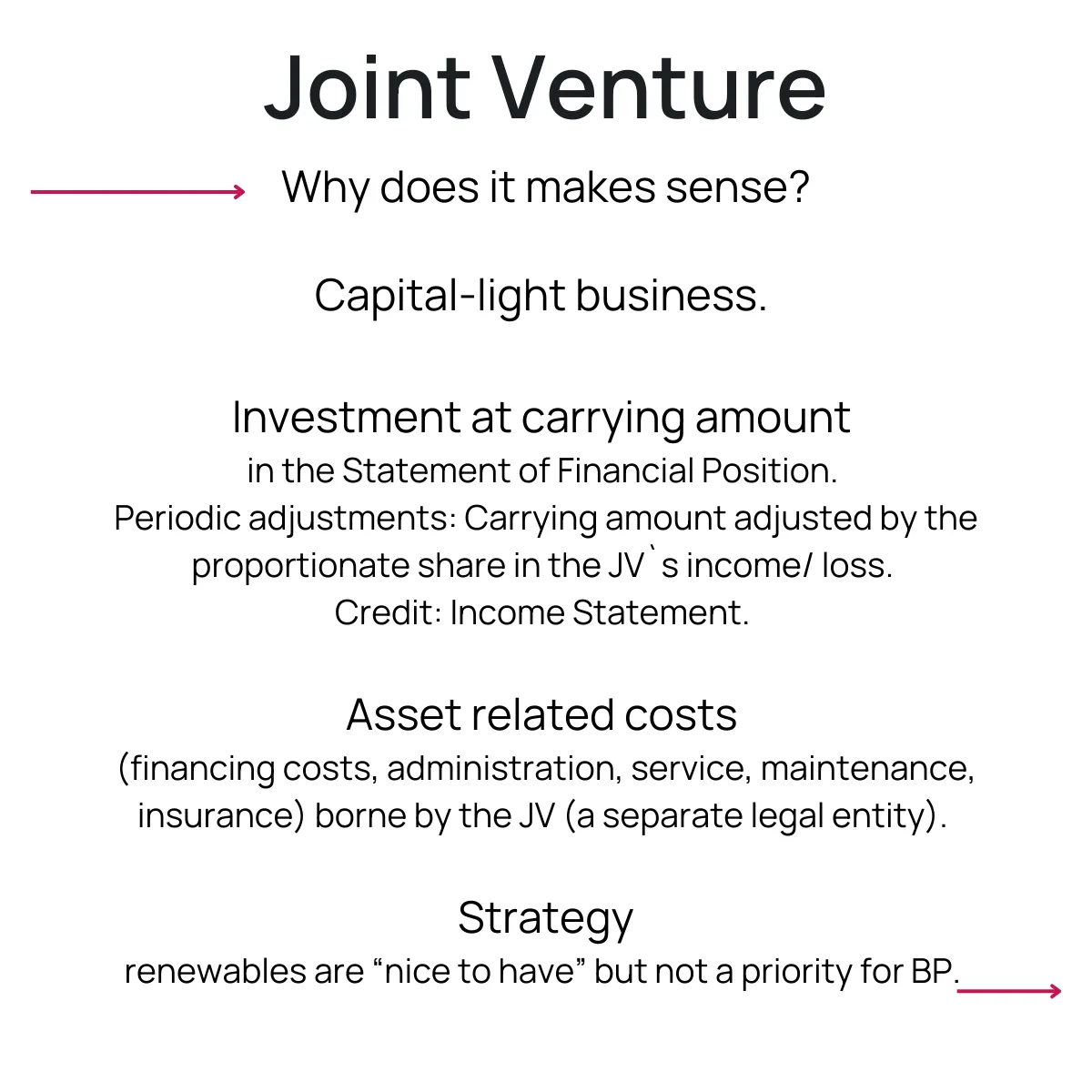

🔹 Asset side – higher return on assets, no depreciation expense in net profit.

🔹 Liability side – lower debt, no interest expense in net profit.

🔹 KPIs: debt to equity ratio, leverage and total debt to total assets.

IFRS 16 largely 'cured' the off-balance sheet policies. Yet, companies still seek for options.

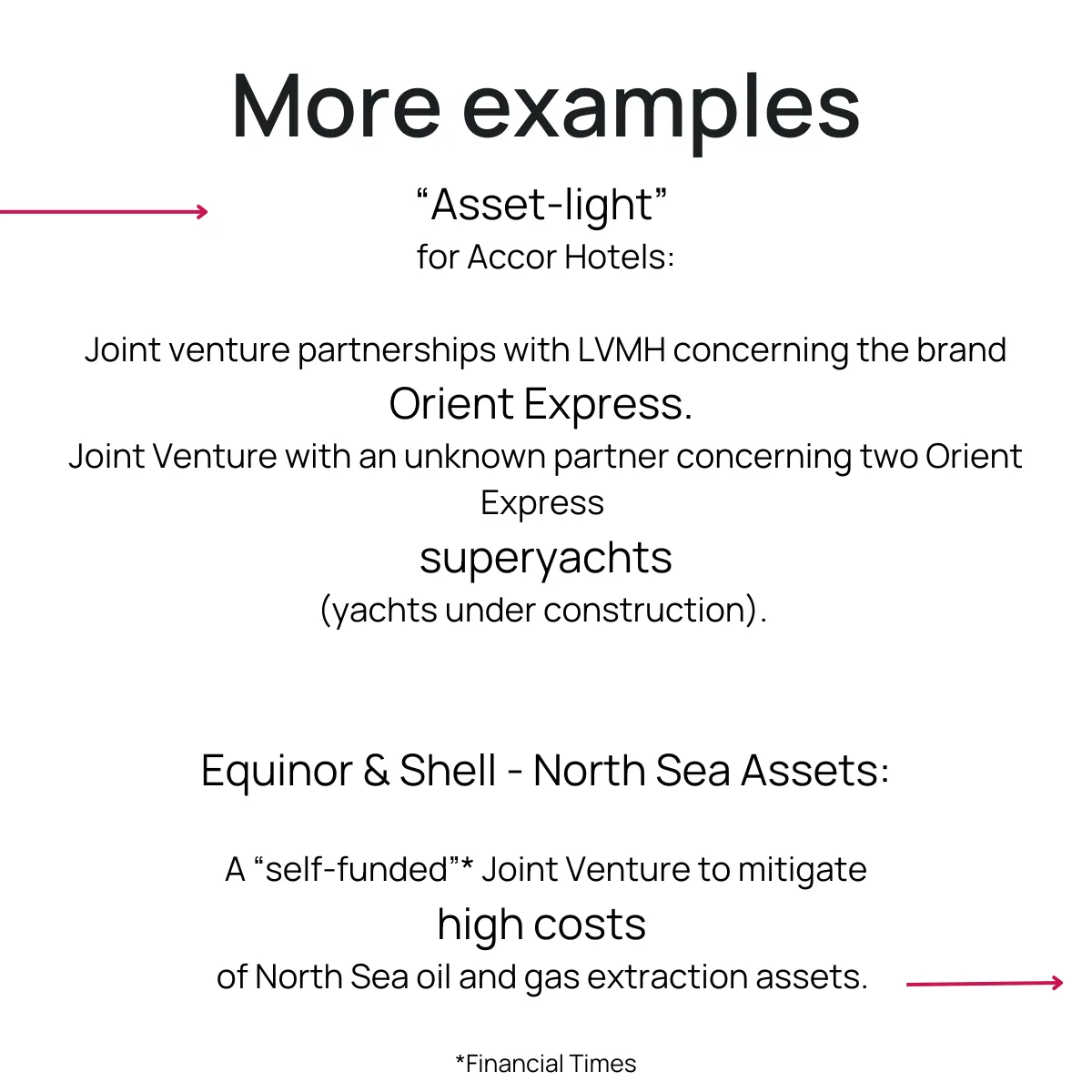

⏩ Swipe to the right to see some real world examples.