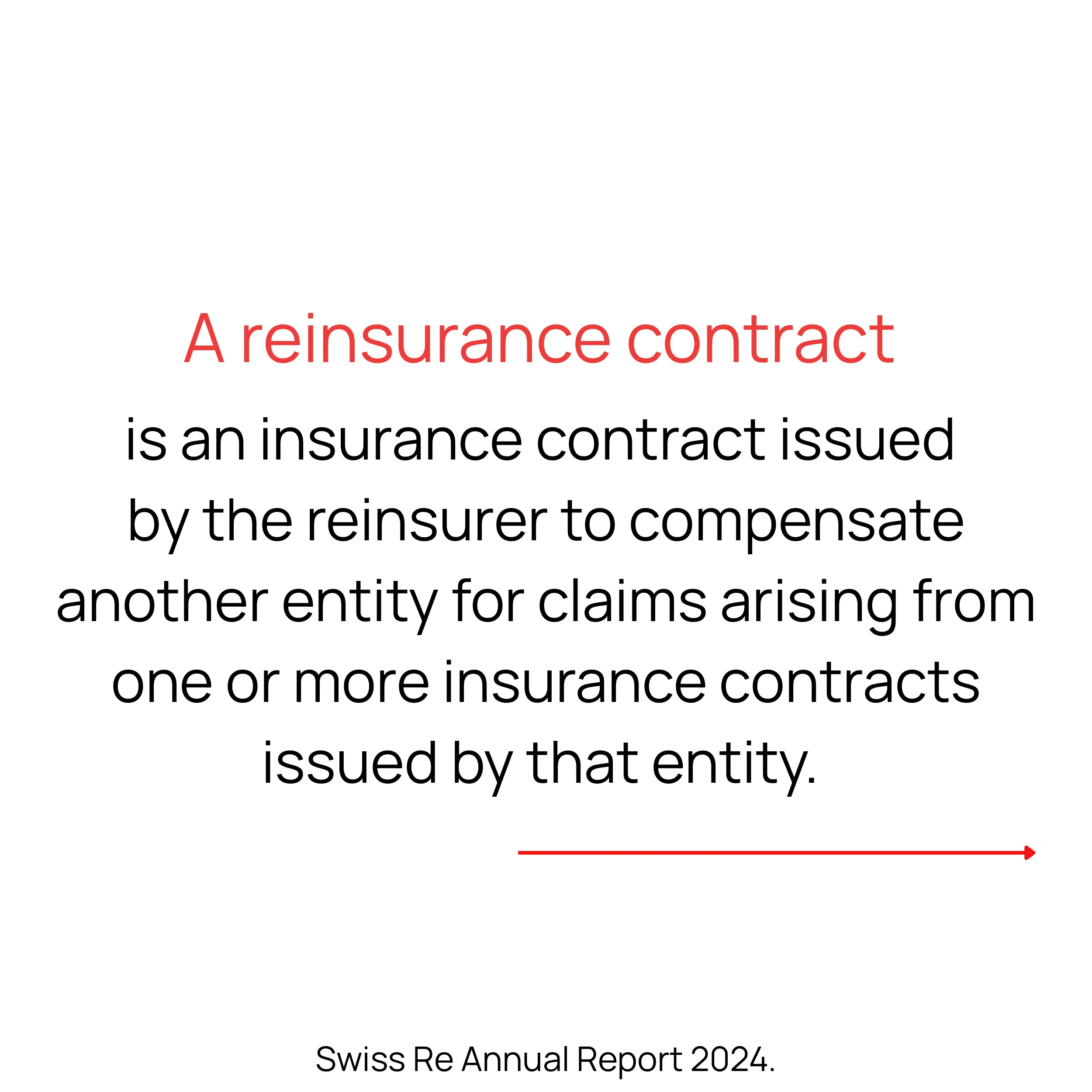

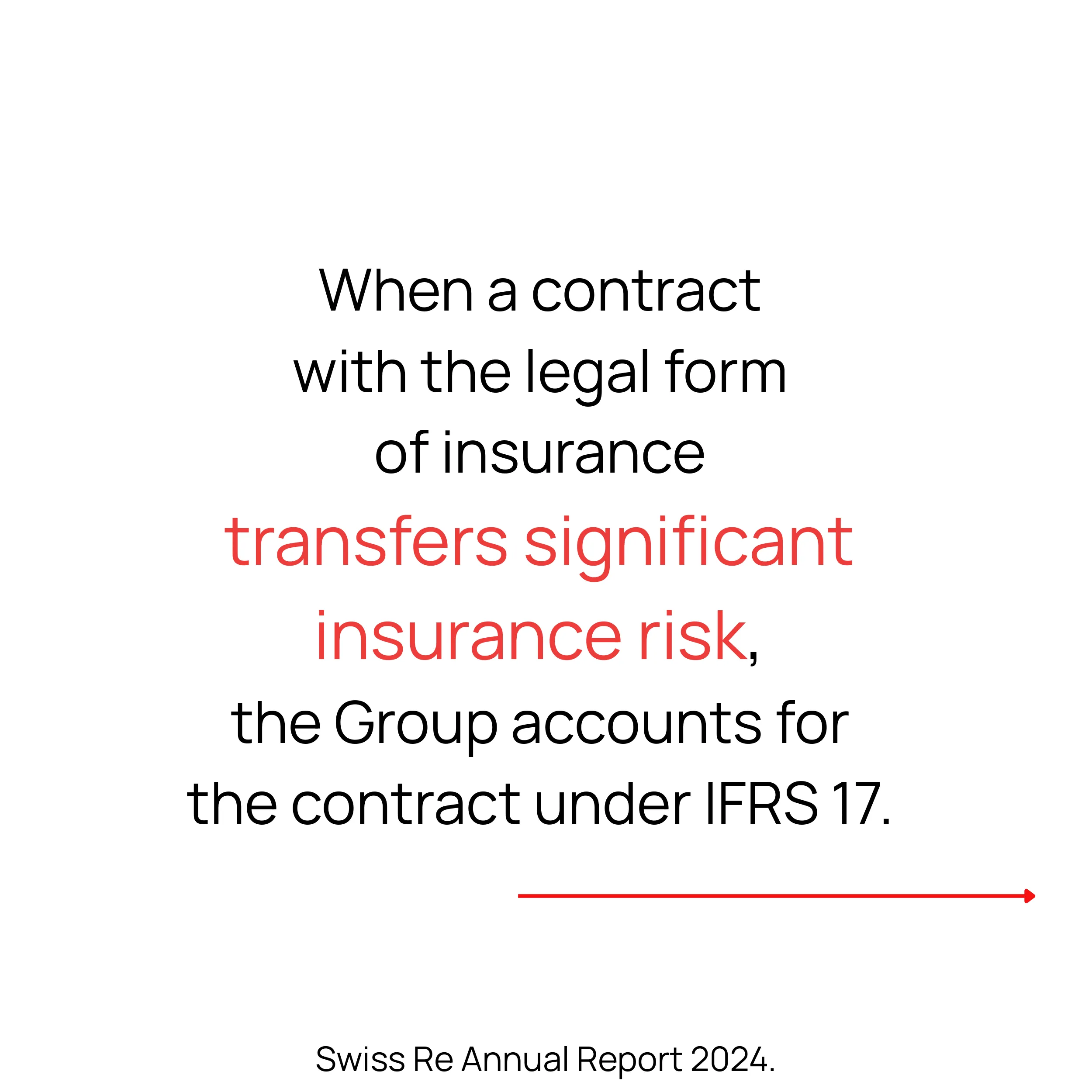

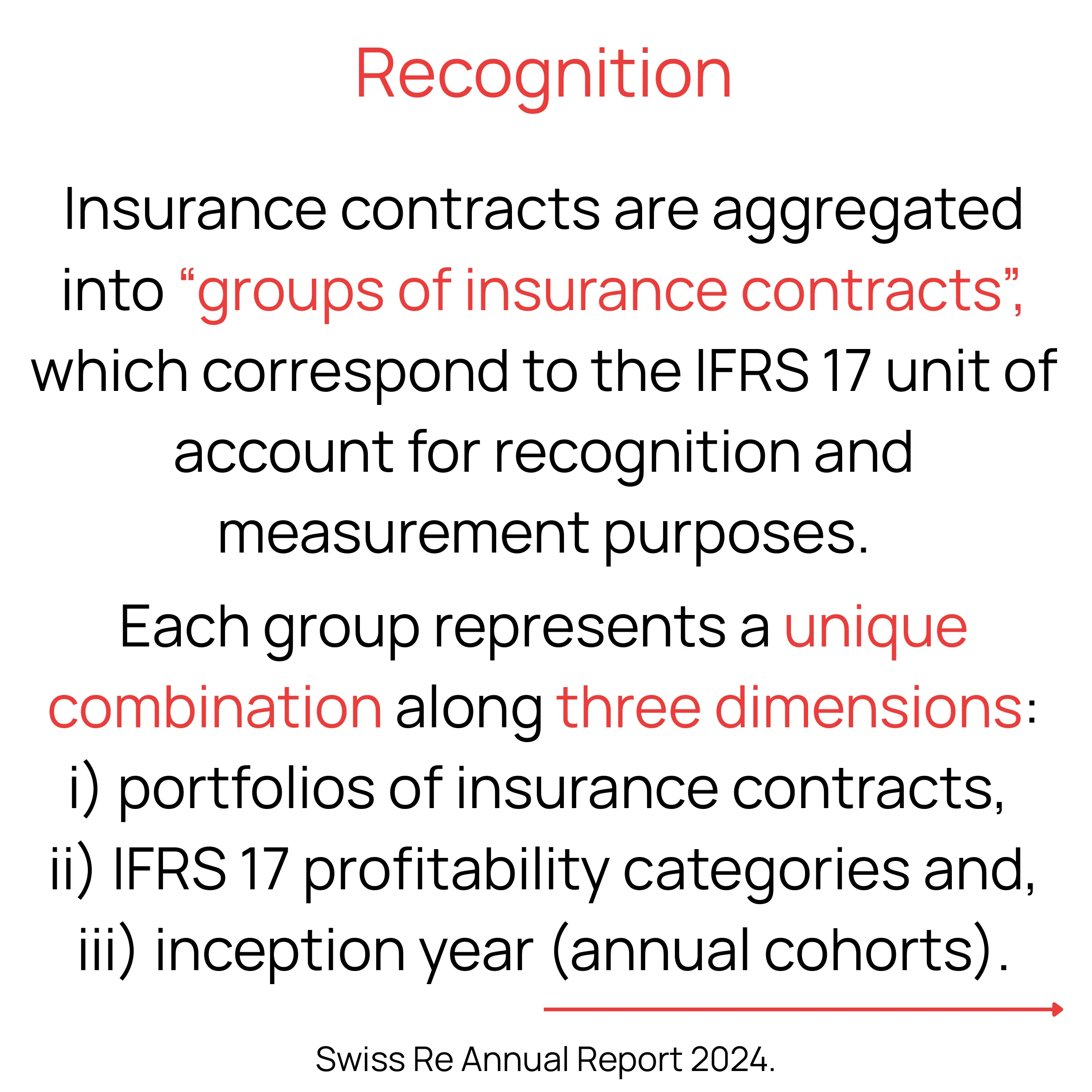

IFRS 17 Insurance Contracts

IFRS 17 establishes principles for the recognition, measurement, presentation and disclosure of insurance contracts.

“The word risk derives from the early Italian risicare, which means to dare. In this sense, risk is a choice rather than a fate."

IFRS 17 Insurance contracts.

📍 Certain kind of insurance or a guarantee might be embedded into almost any contract - a sale, a business combination, a financial instrument - which raises questions about an applicable IFRS standard.

🔸 IFRS 15 Revenue from Contracts with Customers can optionally be applied to:

"Insurance contracts that have as their primary purpose the provision of services for a fixed fee in accordance with paragraph 8 of IFRS 17." In those cases, pricing of the fee and risk are not based on the risk characteristics of a customer.

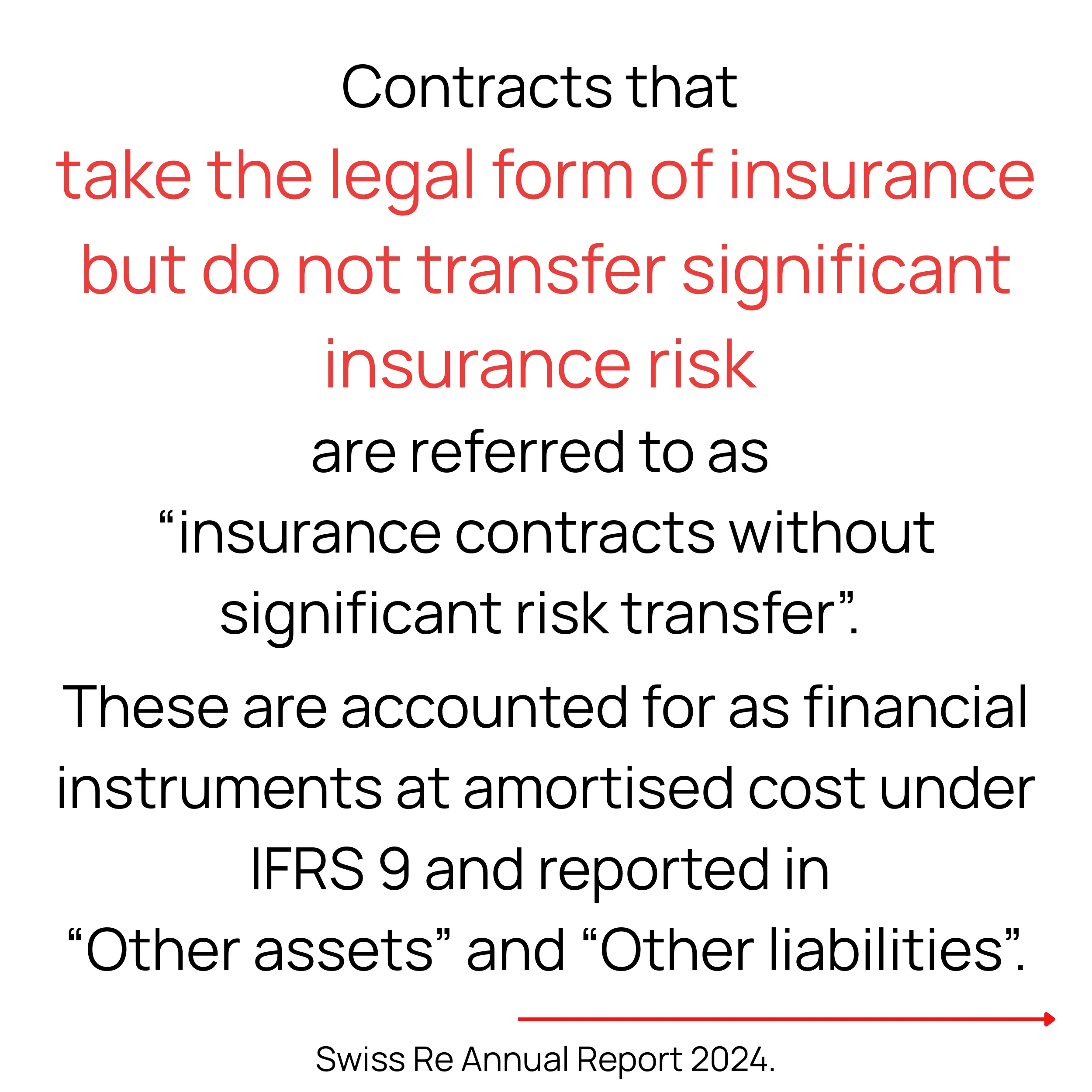

🔸IFRS 9 Financial Instruments applies to:

derivatives that are embedded in contracts within the scope of IFRS 17, unless derivatives themselves are insurance contracts,

investment components that are separated from contracts within the scope of IFRS 17,

an issuer’s rights and obligations under insurance contracts that meet the definition of a financial guarantee contract unless designed by an issuer as insurance contracts,

an entity’s rights and obligations that are financial instruments arising under credit card contracts, or similar contracts that provide credit or payment arrangements excluded from the scope of IFRS 17 by the paragraph 7h),

limited compensations for insured events if an entity elects to to apply IFRS 9 in accordance with the paragraph 8A of IFRS 17.

IFRS 17 Insurance contracts in 15 seconds ⏩

opening quote by Peter L. Bernstein, Against the Gods: The Remarkable Story of Risk via Goodreads