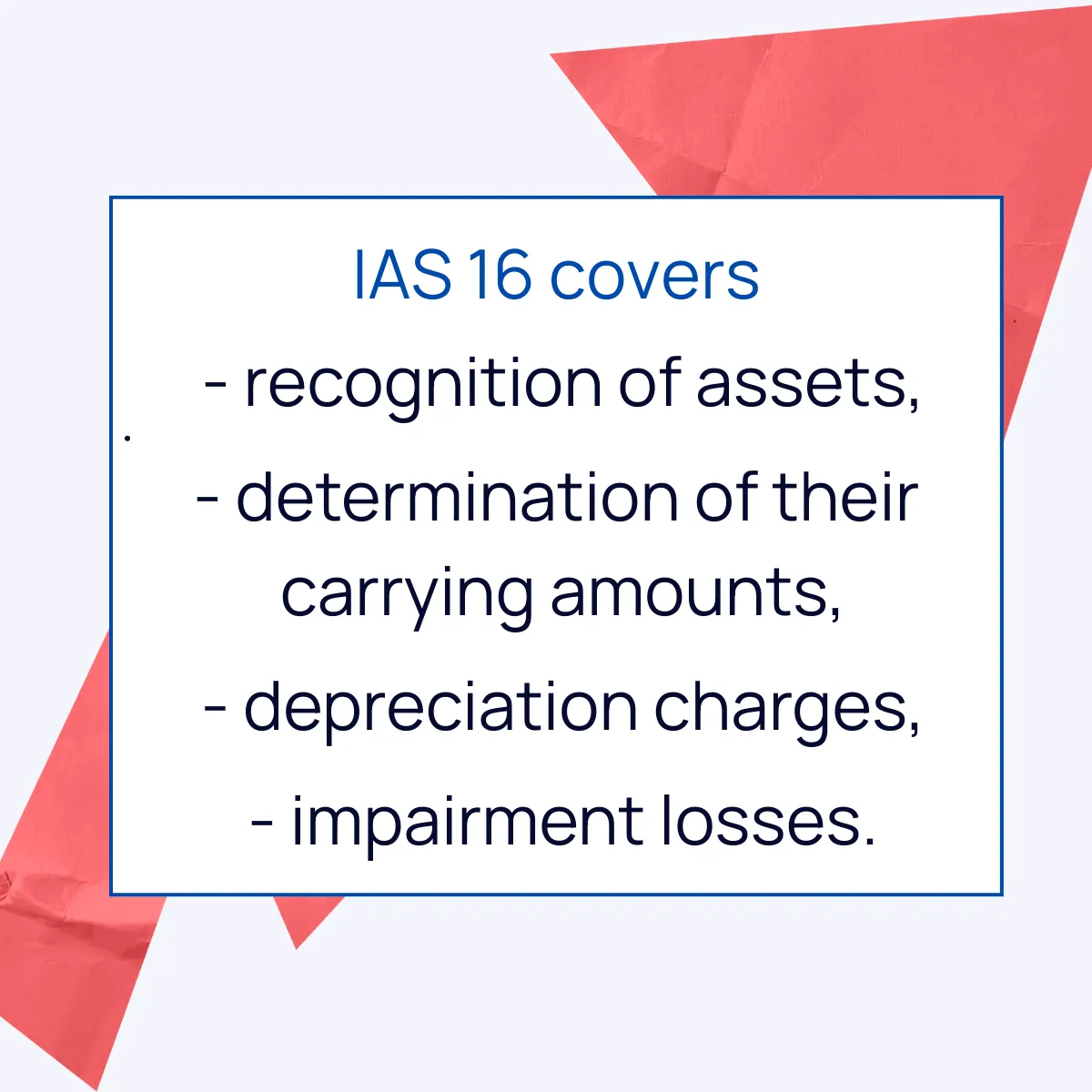

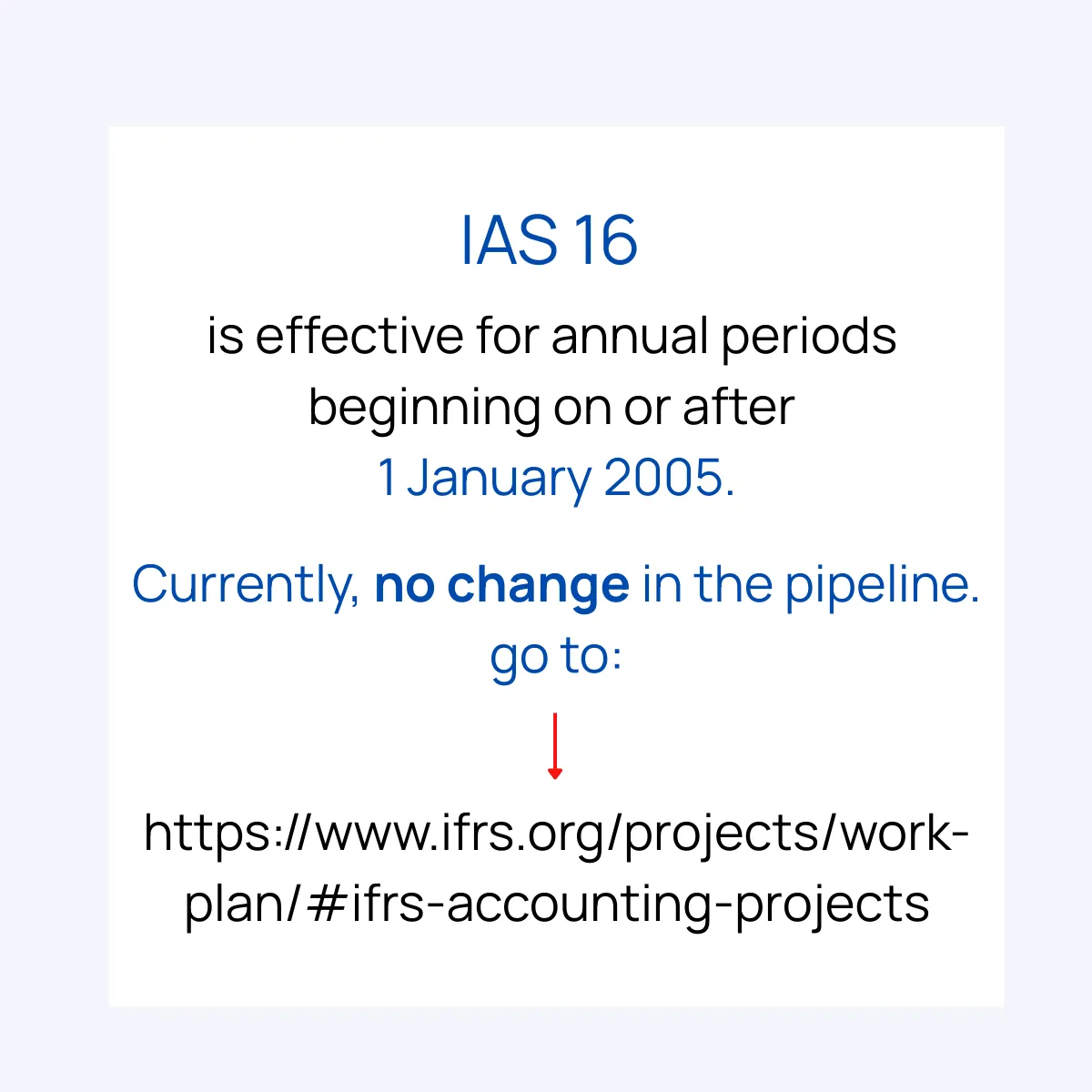

IAS 16 Property, Plant and Equipment

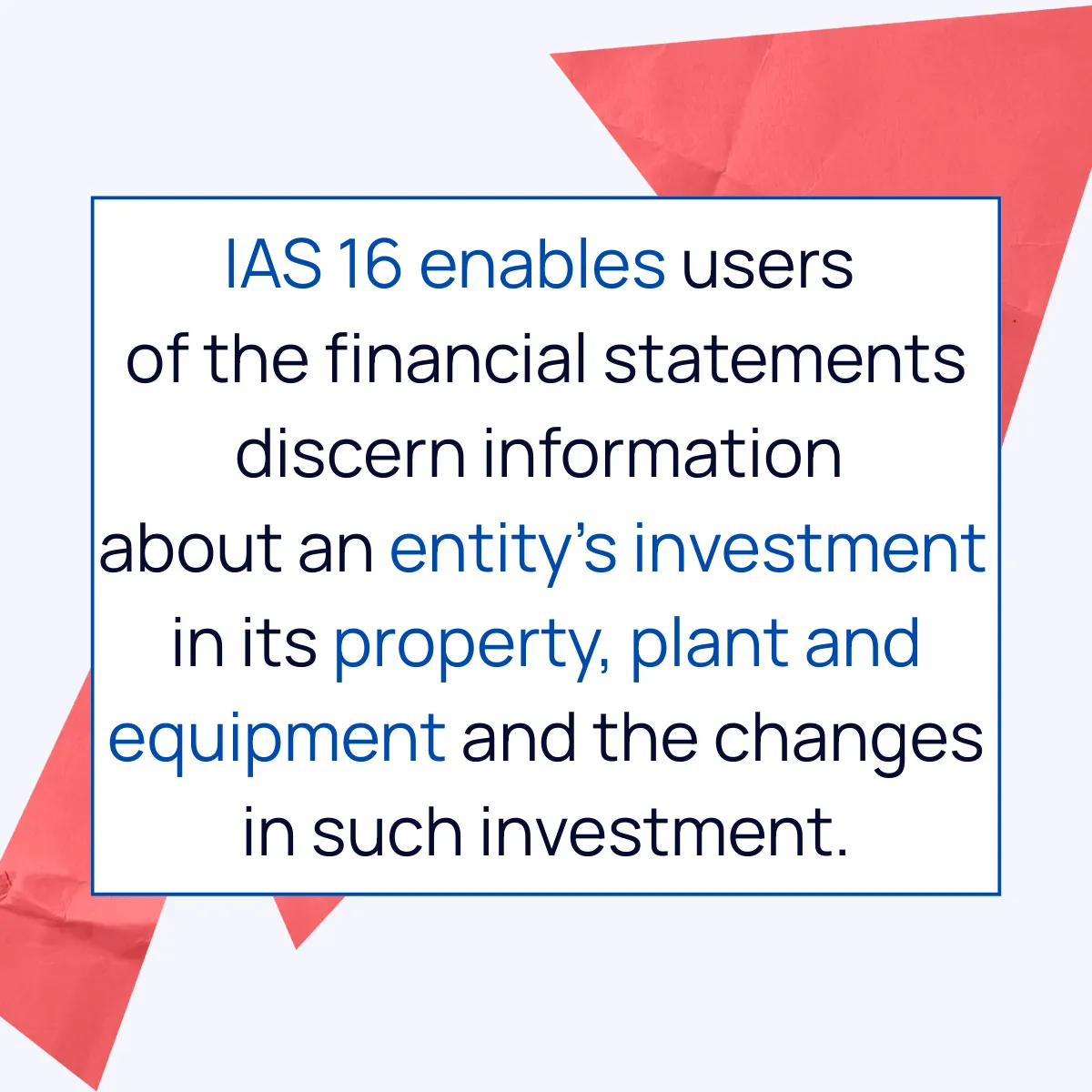

IAS 16 provides information about an entity's investment in its property, plant and equipment and the changes in such investment.

"A property doesn't need to be perfect; it just needs to be yours."

Who does not know the stable, (mostly) straightforward IAS 16 Property, Plant & Equipment?

Apart from the usual carousel I am also sharing links on a few IAS 16-related topics from past IFRIC Agenda Decisions:

1️⃣ Accounting treatment of Core Inventries which were defined are minimum amounts of material necessary to start operations of a production facility.

In one sentence: Shall "core inventories" be accounted for as Inventories or as Property, Plant & Equipment? Depends. Fact patterns in different industries can vary significantly leading to different conclusions.

November 2014: https://shorturl.at/3fE4v

2️⃣ Proceeds from testing in excess of the costs of testing an item of PPE (par. 17 of IAS 16).

In one sentence: Only costs of testing are permitted to be included in the cost of the PPE item. These costs are reduced by the net proceeds from selling items produced during testing.

July 2014: https://shorturl.at/mLv04

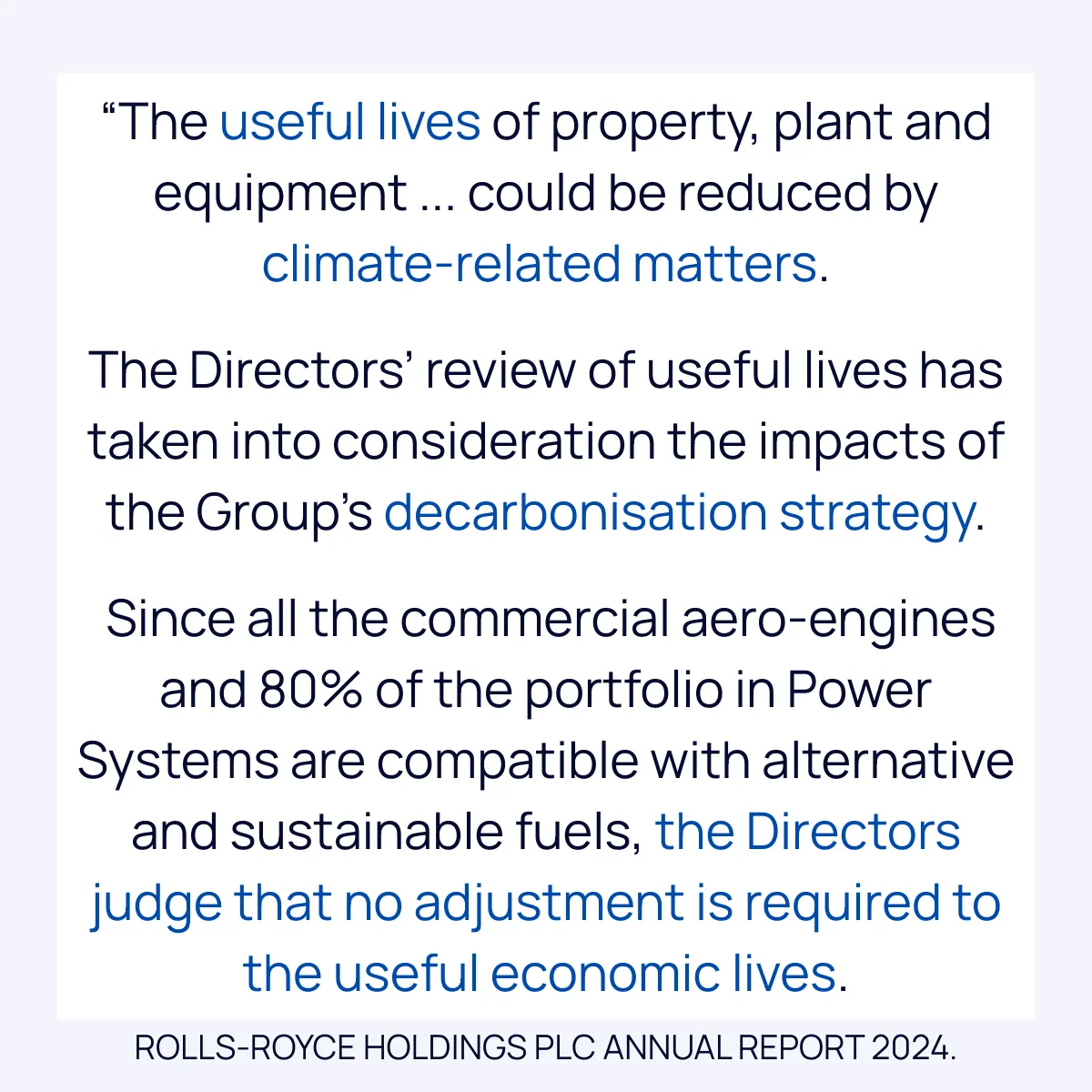

3️⃣ Determination of the useful life of non-removable leashold improvements from November 2019.

In one sentence: Useful life of an asset considers ‘legal or similar limits on the use of the asset, such as the expiry dates of related leases’ (par. 56 b) of IAS 16).

November 2019: https://lnkd.in/eRdVt6jC

headline quote by Linsey Mills, Currency of Conversations via Goodreads.